This is the second of two articles on economic moats. The first part covered intangible assets, cost advantages, and scale. We now cover the other two sources, the ones that are hardest to break once they take hold: switching costs and the network effect.

Same reminder as before. A moat protects a company’s margins, and those margins are what pay and grow the dividend. The stronger the moat, the safer the raise. These two are the stickiest moats of all.

*Disclosure: This is education, not advice. Do your own due diligence.

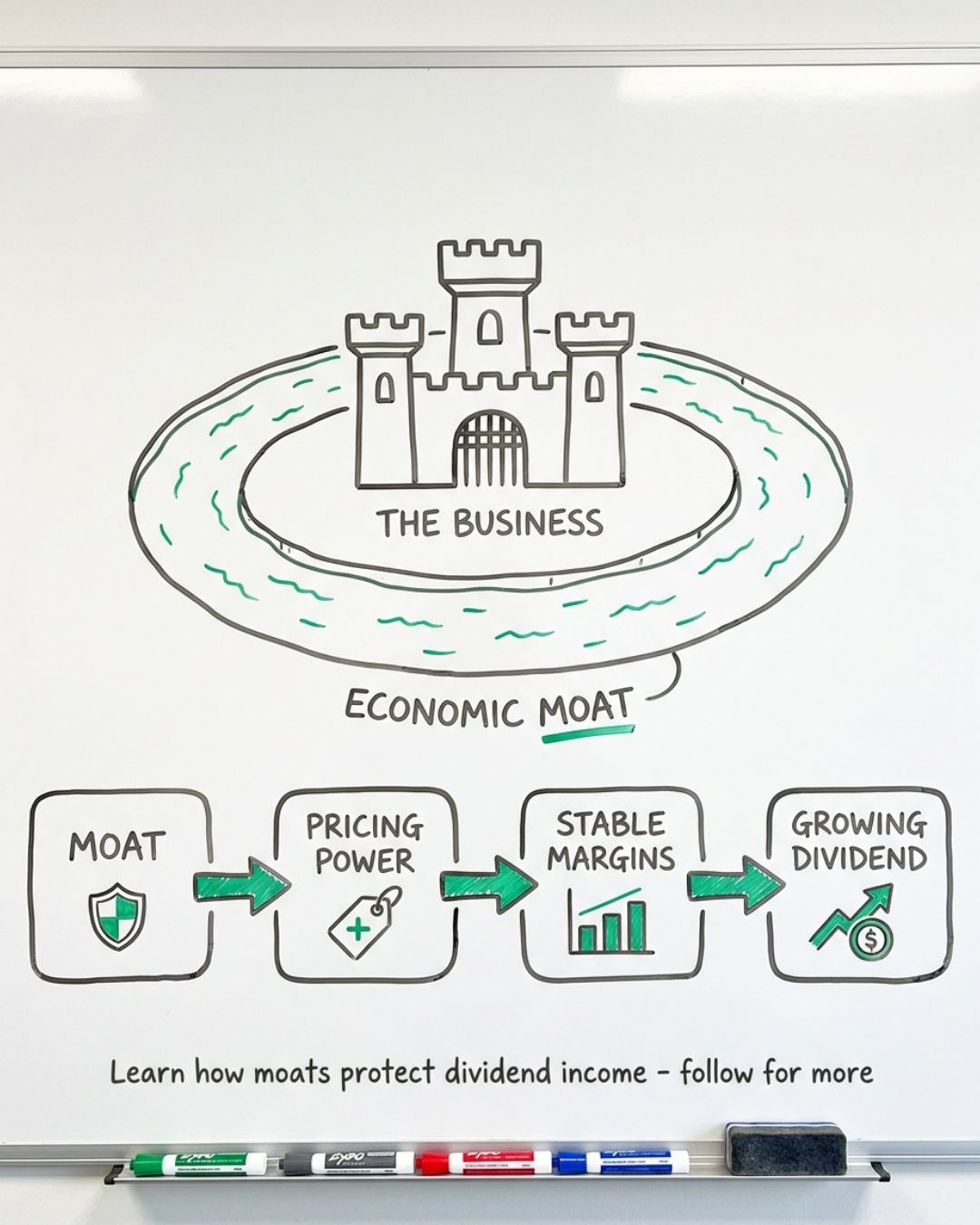

What a moat does for your dividend

At Dividend Stocks Rock, the moat is among the first things we look for in our investment thesis, not the last. It is not about how big a company is. It is about how hard it is to replace.

Here is the chain. A moat creates pricing power. Pricing power protects margins. Protected margins fund a dividend that continues to rise. Switching costs and network effects build that wall about as high as it goes.

Switching costs: when leaving hurts too much

A switching cost is the price your customer pays to walk away. When the price is high enough, customers stay even after a cheaper option appears. That is pricing power you can bank on.

Switching costs come in three flavors.

- Financial. Real money was lost in the move. Canceled contracts, new equipment, lost data, retraining bills.

- Procedural. Time, effort, and risk. Moving to a new system can take months and break things along the way. Most teams decide it is not worth the headache.

- Relational. The human glue. Years of service history, trusted contacts, and habits nobody wants to rebuild.

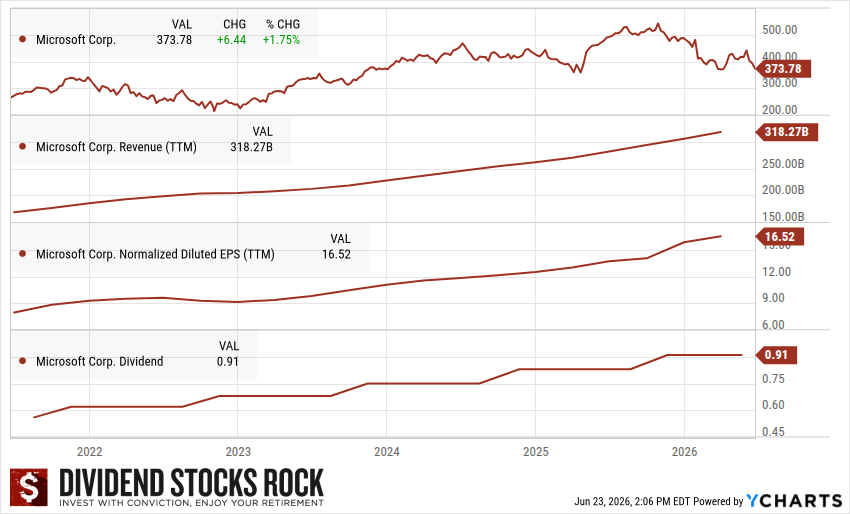

Microsoft is the clearest example anywhere. A company runs its email, documents, spreadsheets, and cloud on Microsoft, and its people have used those tools throughout their careers. Pulling all of that out and retraining everyone is a nightmare most leaders will never sign up for. So they renew, and they pay a little more each year.

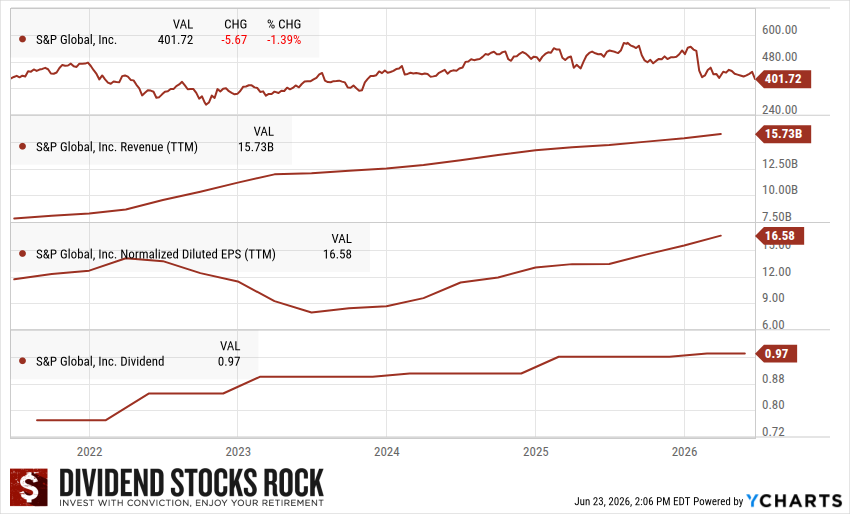

S&P Global is the same idea in the market’s plumbing. Its ratings, indices, and data are wired into how the financial world runs. A bond issuer cannot casually drop its rating agency. An asset manager cannot unplug from the S&P 500 without a hard conversation with clients. That lock-in is why both companies raise prices slightly every year and keep getting paid.

The network effect: every new user makes it stronger

The network effect is the rare moat that grows on its own. Each new user makes the service more valuable to every other user. The product improves the more people use it, and a rival cannot copy that with money alone.

It also comes in three flavors.

- One-sided. More users of the same kind add value for each other. A messaging app is only useful if your friends are on it too.

- Two-sided. Two different groups feed each other. More buyers attract more sellers, which attract more buyers.

- Complementary. A web of products that reinforce one another, so leaving one means leaving them all.

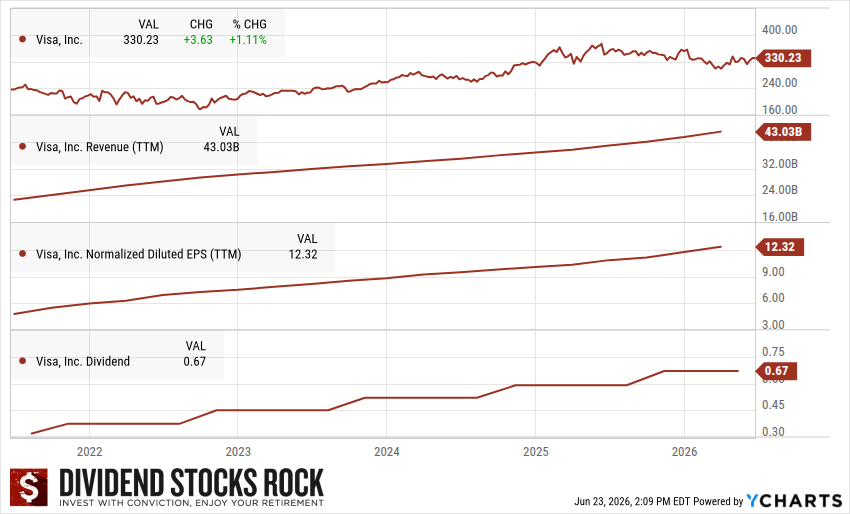

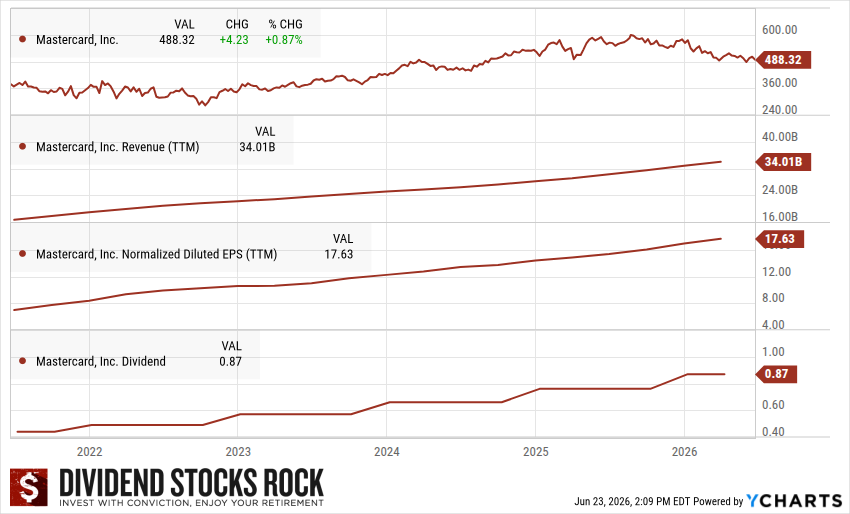

Visa and Mastercard are textbook two-sided networks. More cardholders pull in more merchants. More merchants pull in more cardholders. That loop has been spinning for decades, and a new entrant cannot buy its way onto both sides at once. Both businesses run light on assets and heavy on margin, which is exactly why the dividend keeps growing.

How these moats show up in the dividend triangle

You do not have to take a moat on trust. It leaves a mark.

A switching-cost or network business tends to show steady revenue, smooth earnings, and a dividend that rises without pushing the payout ratio higher. When customers cannot easily leave, the company raises prices slightly each year and maintains its margins through the cycle.

If the moat story is loud but the margins swing and the dividend growth stalls, the moat is thinner than the pitch. The triangle settles the argument.

When the moat slips

No moat lasts forever. A network is only a fortress as long as everyone still wants to be inside it. Switching costs fade the moment a rival removes the friction. Plenty of businesses looked untouchable right up until a new model made leaving easy.

So we re-check the moat the same way we check the dividend. The day the margins start slipping is the day the thesis needs a second look, long before the dividend is ever at risk.

Five moats, one question

Across these two articles, we have walked through all five sources of a moat: intangible assets, cost advantages, economies of scale, switching costs, and network effects.

When you analyze a stock, ask one question. Does it have a moat, and what is it built on? Answer that, and you can judge how long a company can defend its profits, and how safe its dividend really is. Everything else is detail.

Skip the Screening and Start With 300 Strong Candidates

Companies with real moats are the backbone of a dividend growth portfolio. I built the Dividend Rock Stars List to help you find them faster. It tracks about 300 dividend stocks with grow ing trends, already sorted, so you can spot strong candidates without hours of screening.

ing trends, already sorted, so you can spot strong candidates without hours of screening.

Enter your name and email below, and I will send the instant download straight to your mailbox.

Leave a Reply