This is the first of two articles on economic moats. We cover three of the sources that build one: intangible assets, cost advantages, and scale. The next part covers the other two: switching costs and network effects.

First, why does this matter to a dividend investor? A moat protects a company’s margins. Healthy margins are what pay and grow the dividend. Find the moat and you find the reason a payout can keep rising for twenty years. Miss it and you are guessing.

*Disclosure: This is education, not advice. Do your own due diligence.

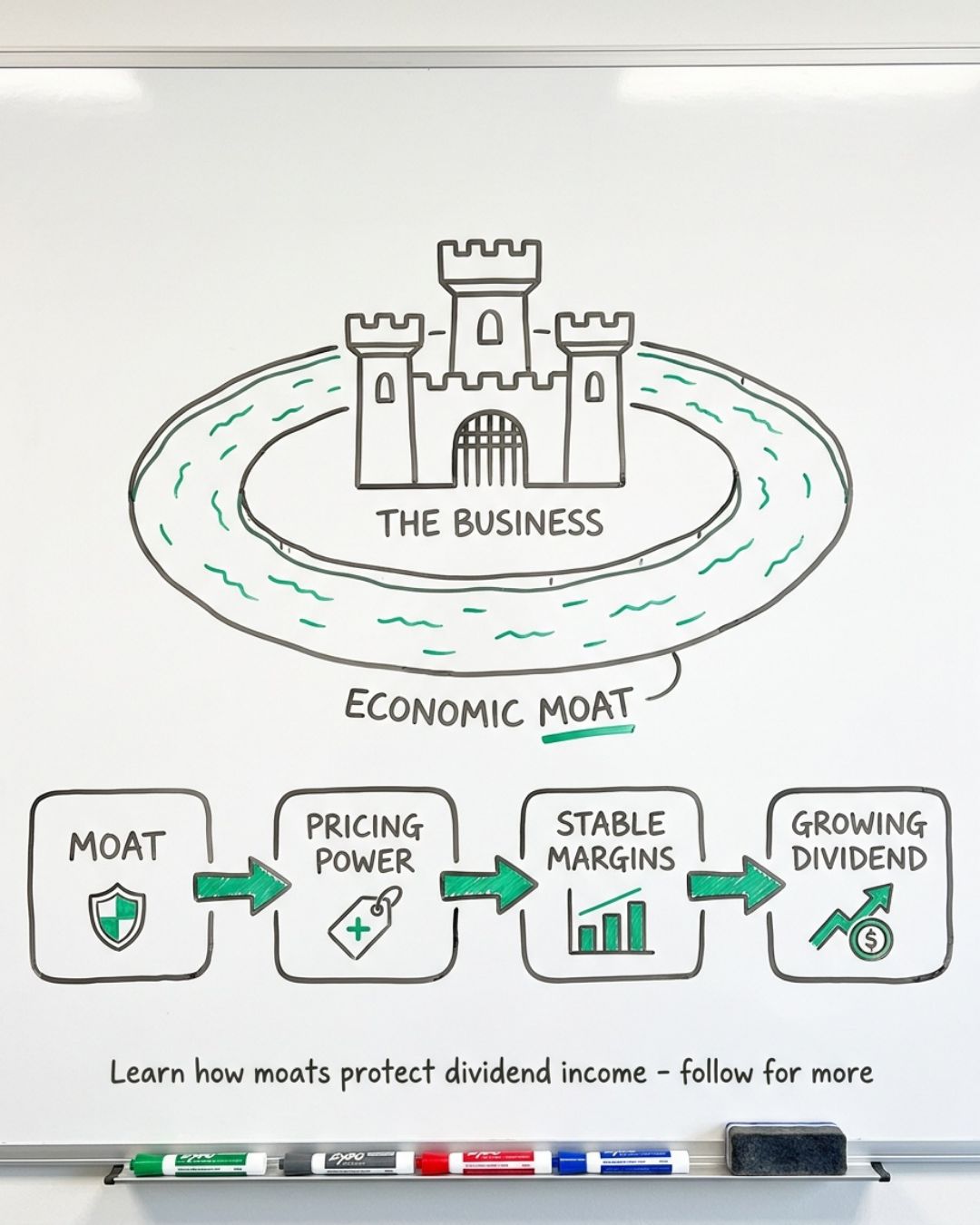

What a moat does for your dividend

At Dividend Stocks Rock, we treat the moat as part of the investment thesis, not a nice-to-have. A moat is not about size. It is about being hard to replace.

The chain is simple. The moat creates pricing power. Pricing power holds up margins. Steady margins fund a rising dividend. A long, smooth dividend growth streak is often a moat showing up in the numbers.

Intangible assets: brands, secrets, and know-how

Intangible assets are the moats you cannot touch. Brand equity, intellectual property, and proprietary technology. They are hard to measure and harder to copy.

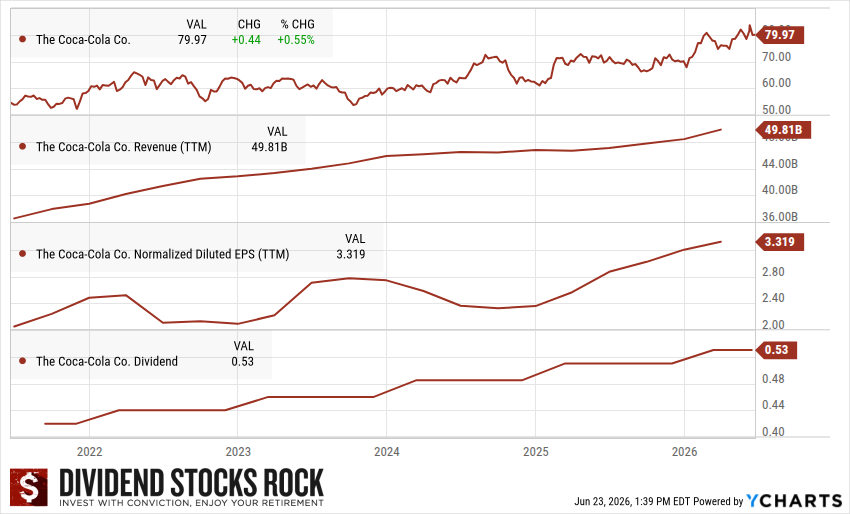

Start with the brand. A strong brand buys pricing power. Coca-Cola can charge more than a generic cola, and people still reach for the red can. It pairs that brand with a real trade secret, the formula itself, which is intellectual property no competitor can legally copy.

McDonald’s is the same idea on a different menu. Open a no-name burger joint, and you fight for every customer. Hang the golden arches and the line forms on day one. That brand pull is why McDonald’s has raised its dividend for decades.

A strong brand does not guarantee profits, though. The point is pricing power, not fame. Plenty of famous names operate on thin margins and have shaky payouts.

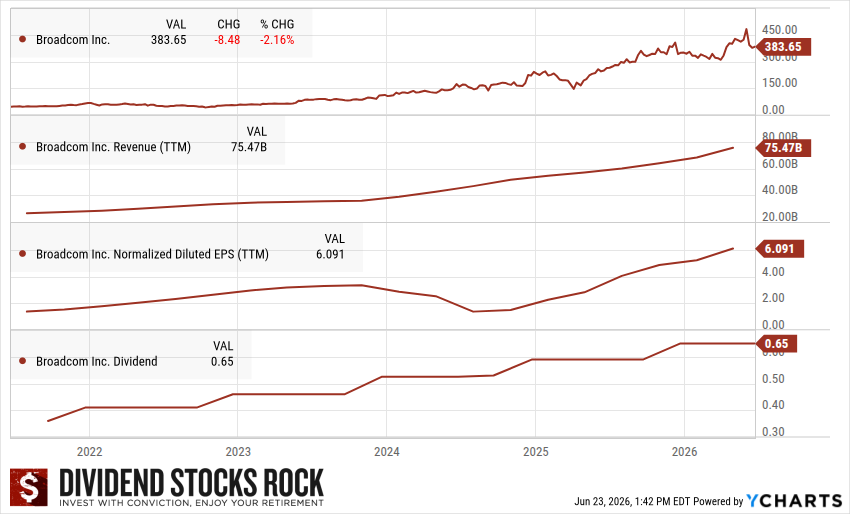

Proprietary technology is the third intangible. A process or design that rivals cannot easily reproduce. Broadcom designs the specialized chips that run modern networks, smartphones, and data centers, then layers hard-to-replace infrastructure software on top. That mix of silicon and software fuels one of the fastest dividend growth records in tech.

Intangibles can vanish

Here is the catch with intangibles. They can disappear fast. Before Michael Jordan signed with Nike, Converse was the basketball shoe leader. Nike loaded the deal with royalties and perks, landed Jordan, and rewrote the market. Today, Converse is a small piece of Nike, worth a fraction of what it once commanded. A brand moat is real until the day it is not.

Cost advantage: be the low-cost winner

A cost advantage means you make the product or deliver the service cheaper than anyone else. That edge plays out two ways.

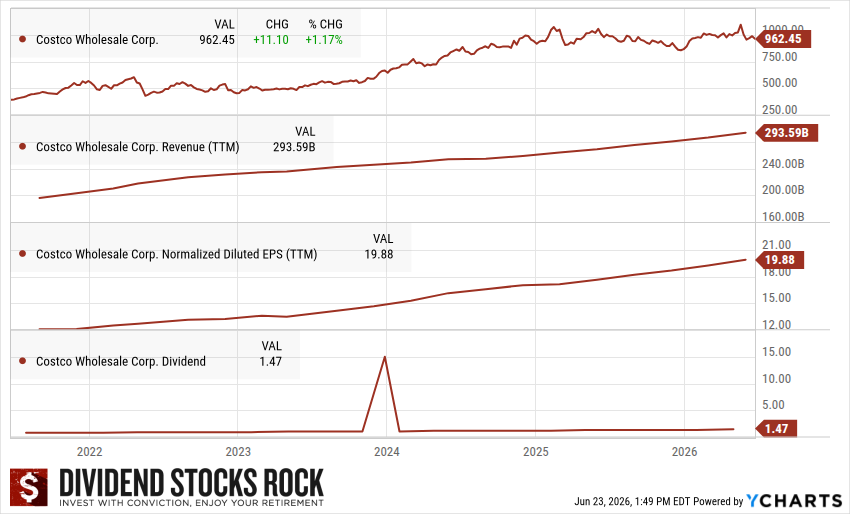

Crush on price. Produce cheaper, sell cheaper, take share. Costco is the model. It acts as the largest customer for many suppliers, secures the best prices, and passes the savings on to members. Low prices bring members, membership fees fund the model, and the dividend keeps climbing.

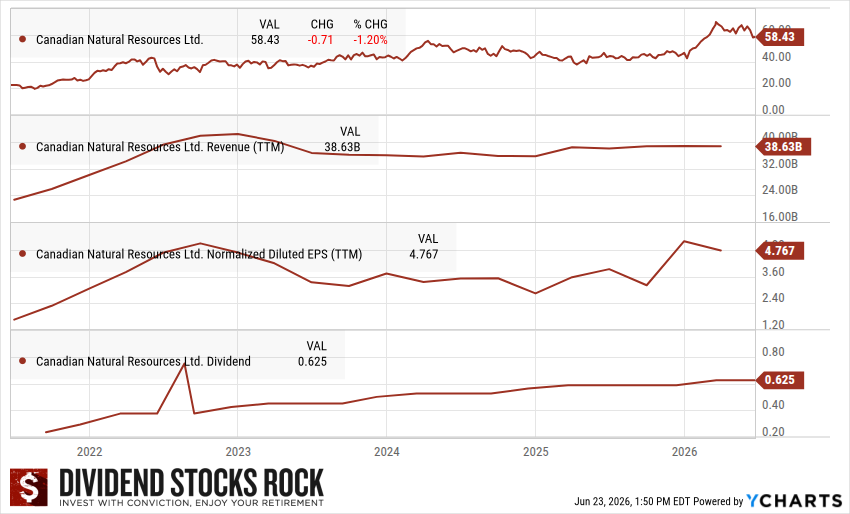

Match the price, keep the difference. When the market sets one price, the low-cost producer simply earns fatter margins. Canadian Natural Resources is a clean energy example. Its long-life, low-decline reserves let it pump oil and gas at a low cost, ramp up when prices rise, and stay profitable when they fall. That cost edge turns CNQ into a cash flow machine.

Walmart runs the same low-price playbook in retail. In transport, the railroads are the cheapest way to move freight across land, which is part of why Canadian National and Canadian Pacific are such durable businesses.

A cost advantage is also a weapon. “Your margin is my opportunity,” Jeff Bezos once said. Barnes & Noble looked safe until Amazon showed up with a leaner model and a relentless focus on cost. Barnes & Noble survived, but it never thrived again.

Efficient scale: markets that fit only a few

Efficient scale is the quiet moat. It shows up when a market is too small to support more than one or a few players, so nobody bothers to build a competitor.

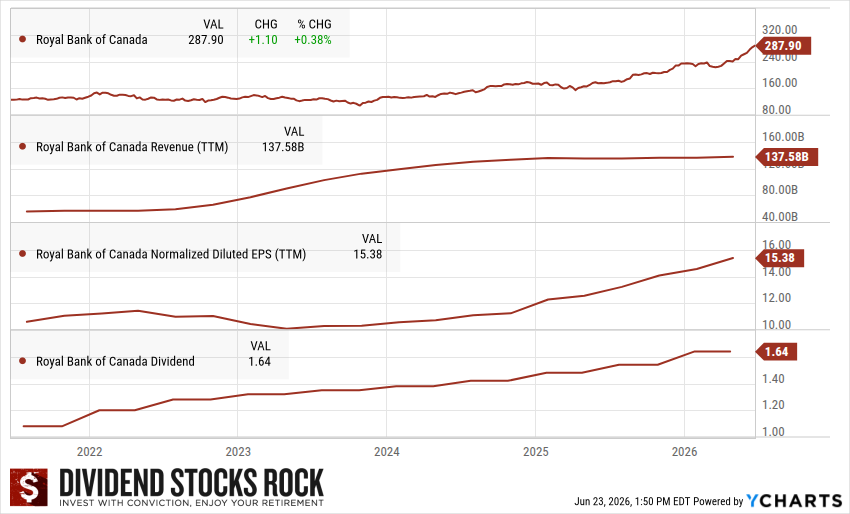

Canadian banking is the textbook case. The Big Six run an oligopoly that controls most of the country’s banking, and the rules make it almost impossible for a seventh national challenger to emerge. Royal Bank sits at the top of that structure with the strongest profile of the group.

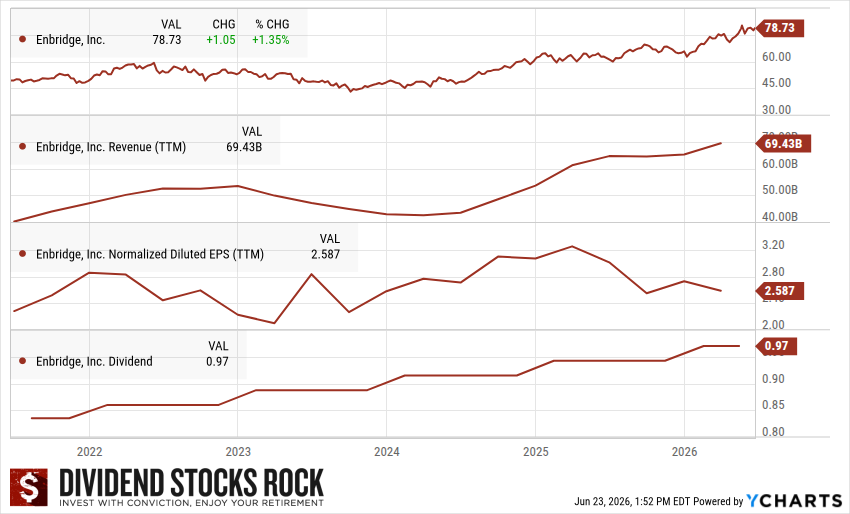

Railroads and pipelines share the trait. There is no point in laying a second rail line or pipeline beside one that already works. The cost is prohibitive, and both routes would bleed money. That is why a pipeline like Enbridge can move a huge share of the continent’s energy and keep paying a growing dividend.

One caution. Efficient scale invites regulation. Governments dislike markets with little competition, so price caps and oversight are part of the territory. It is a strong moat, not a free pass.

How these moats show up in the dividend triangle

You do not have to take a moat on trust. It leaves a mark.

A brand, a cost edge, or a scale advantage all land the same way in the numbers: steady revenue, smooth earnings, and a dividend that rises without pushing the payout ratio higher. Real pricing power means a company lifts prices a little each year and keeps its margins through the cycle.

If the moat story is loud but the margins swing and the dividend growth stalls, the moat is thinner than the pitch. The triangle settles the argument.

Find the moat before you buy

When you analyze a stock, start with one question. Does it have a moat, and what is it built on? Switching costs, the network effect, a brand, a cost advantage, scale, or some mix of them?

Answer that and you can judge how long a company can defend its profits, and how safe its dividend really is. Everything else is detail.

Skip the Screening and Start With 300 Strong Candidates

Companies with real moats are the backbone of a dividend growth portfolio. I built the Dividend Rock Stars List to help you find them faster. It tracks about 300 dividend stocks with growi ng trends, already sorted, so you can spot strong candidates without hours of screening.

ng trends, already sorted, so you can spot strong candidates without hours of screening.

Enter your name and email below, and I will send the instant download straight to your mailbox.

Leave a Reply