Railroads are a textbook sector for dividend investors. Wide moats, irreplaceable networks, pricing power above inflation, and cash flow that keeps showing up quarter after quarter.

But “own a railroad” is not a strategy. You need to pick the right one.

Three names dominate the North American market: Canadian Pacific Kansas City (CP), Canadian National Railway (CNR), and Union Pacific (UNP). Same industry, same moat, three different profiles.

Here is how I rank them, and why.

Disclosure: I own CNR in my portfolio. I do not own CP or UNP. This is education, not advice. Do your own due diligence.

How I compare railroads

Before I rank anything, I run every candidate through the same four-step checklist:

- The Dividend Triangle: revenue growth, EPS growth, and dividend growth over five years. All three need to be positive and aligned.

- Dividend safety: payout ratio, cash payout ratio, and dividend history. I want room to grow and a clean track record.

- Balance sheet: debt to EBITDA, credit score, and current ratio. A leveraged railroad in a recession is not fun to hold.

- Yield vs. history: if the forward yield sits above the 5-year average, the stock may be offering better income value than usual.

No spreadsheet tricks. Just discipline.

The scorecard

| Metric | CP (CPKC) | CNR | UNP |

| DSR PRO Rating | 4 | 4 | 3 |

| Dividend Safety Score | 3 | 4 | 3 |

| Forward Yield | 0.92% | 2.40% | 2.07% |

| Average 5-Yr Yield | 0.80% | 2.15% | 2.35% |

| 5-Yr Revenue Growth | 14.61% | 4.62% | 4.89% |

| 5-Yr EPS Growth | 2.98% | 8.63% | 9.15% |

| 5-Yr Dividend Growth | 4.38% | 8.49% | 6.61% |

| Payout Ratio | 19.22% | 46.78% | 45.35% |

| Consecutive Years of Dividend Increases | 1 | 30 | 17 |

| Chowder Score | 5.30 | 10.89 | 8.68 |

| Credit Score | 90 | 89 | 74 |

Source: Dividend Stocks Rock stock cards, Q1 2026 review.

Now, let me walk through why each one lands where it does.

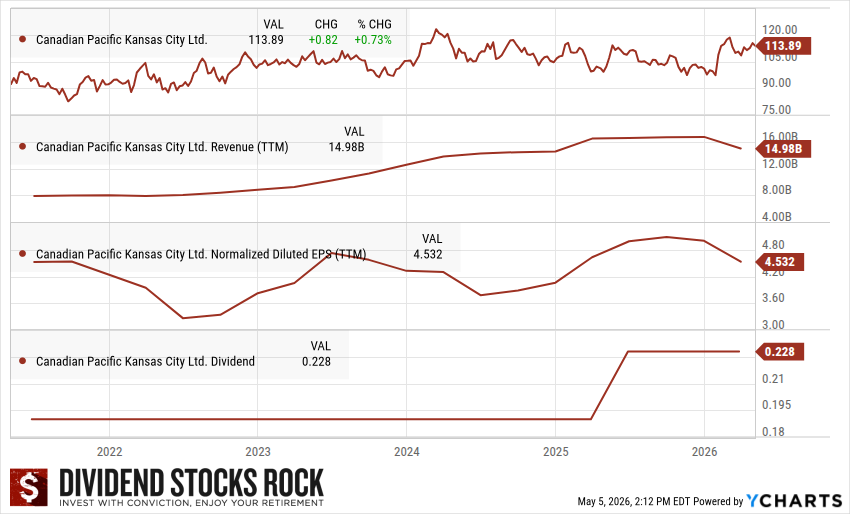

#3: Canadian Pacific Kansas City (CP)

Investment thesis: CPKC is a capital appreciation story, not a dividend story. Management runs the business for total return rather than a growing paycheck.

CPKC has the best growth story in the group. The 5-year revenue number is inflated by the Kansas City Southern acquisition, but the thesis is real: a single-line network linking Canada, the United States, and Mexico, with access to Gulf Coast ports and Mexican trade flows no competitor can match. This integration is now delivering gains in the operating ratio. Cash flow benefits from demand for bulk commodities (grain, fertilizer, metallurgical coal).

So why is it third?

Because CP is not a dividend grower. Management has paused dividend growth multiple times over the past decade. The current dividend streak is one year. The 5-year dividend growth rate is 4.40%, below both CNR and UNP.

If you want a dividend paycheck that grows every year, it does not belong on your shortlist.

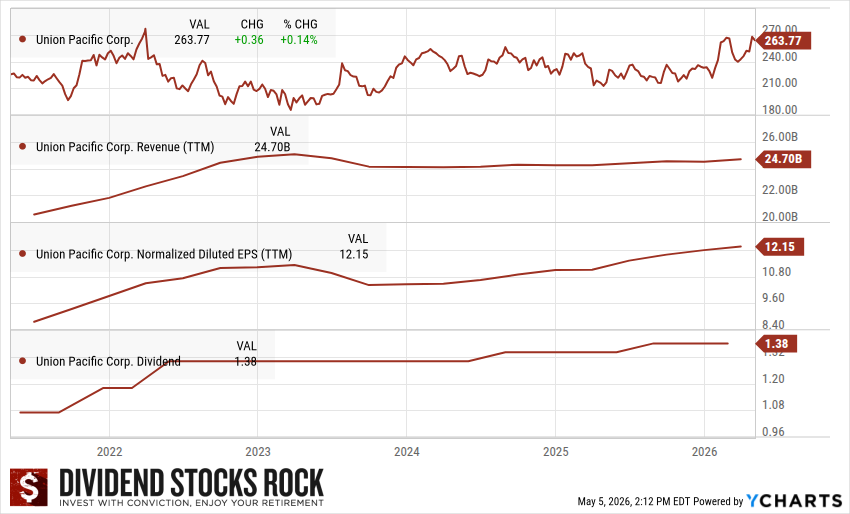

#2: Union Pacific (UNP)

Investment thesis: UNP owns an irreplaceable Western U.S. rail network with exclusive access to Asia trade flows through West Coast ports and all six U.S. to Mexico gateways. Coal volumes are in secular decline, but other goods are rebounding. The proposed Norfolk Southern acquisition could add $2.75B in synergies if regulators approve it (decision expected by early 2027), but adds integration risk and regulatory uncertainty. The business is cyclical and tied to the global economy.

The dividend story is where it loses points.

UNP used to be a dividend growth machine. Since 2022, the policy has been hectic. A pause during COVID. A generous post-COVID increase. Another pause in 2023. Two 3% increases in 2024 and 2025. The 3-year dividend growth rate has slowed to 1.75%. The forward yield sits below the 5-year average, suggesting the stock is not offering better income than usual.

UNP also has the lowest credit score and the highest debt-to-equity ratio of the three.

Solid business. Choppy dividend growth policy. That combination keeps it out of first place.

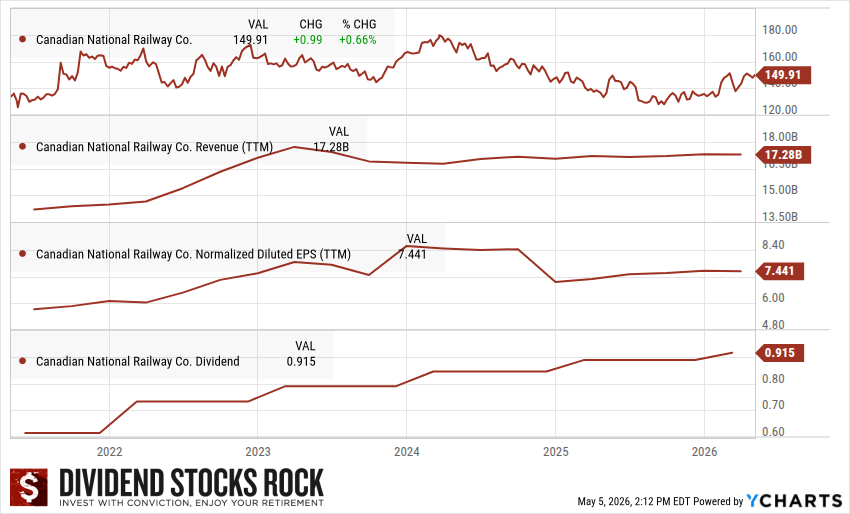

#1: Canadian National Railway (CNR)

Investment thesis: CN runs the only three-coast rail network in North America, connecting the East, the West, and the Gulf of Mexico via the U.S. Midwest. Precision scheduled railroading delivers industry-leading efficiency, and exclusive access to the Port of Prince Rupert is a structural advantage for trade between Asia and North America. Growth comes from pricing power above inflation, new customer projects, and intermodal expansion. 2025 was soft on tariff-induced industrial weakness, and 2026 guidance points to flattish volume with stronger EPS growth, implying continued margin gains in a muted demand environment.

CNR wins on the dividend triangle and the dividend history.

The triangle is balanced: 4.62% revenue growth, 8.63% EPS growth, 8.49% dividend growth over five years. The dividend has been raised every year since 1996. That is 30 consecutive years of increases through recessions, rail strikes, and pandemics. The forward yield sits at 2.40%, above the 5-year average of 2.15%. That is a signal the stock may be offering better income value than usual.

Payout ratios are reasonable (46.78% classic, 61.84% cash), margins are strong (ROE 22.15%, ROIC 9.26%), and the balance sheet carries an investment-grade credit score of 89. CNR also runs the lowest beta of the three (0.99), which matters when the economy wobbles.

The watch-item: management slowed the dividend growth rate to 5% in 2025 and announced a 3% increase for 2026. If that trend continues, the Dividend Safety Score could be downgraded in 2027. I am watching the next two dividend announcements.

For now, CNR is the railroad I want in a dividend growth portfolio.

The verdict

If you want one railroad for dependable dividend growth, CNR is my pick.

If you want growth optionality and you do not need the income, CP is worth a look.

If you want world-class margins but you can live with a choppy dividend policy, UNP fits.

All three are great businesses. Only one fits a dividend growth thesis without compromise.

Leave a Reply