In 2016, I made a life-changing decision: I took a sabbatical, put my family in a small RV, and drove to Costa Rica.

Upon my return in 2017, I officially quit my job as a private banker at National Bank and started working full-time on my baby: Dividend Stocks Rock. I also decided to manage my pension account held at the National Bank. I’ve built this portfolio publicly since 2017 to make a real-life case study. I decided to invest 100% of this money in dividend growth stocks.

In August 2017, I received $108,760.02 in a locked retirement account. This means I can’t add capital to the account, and growth is only generated through capital gains and dividends. I don’t report this portfolio’s results to brag about my returns or to tell you to follow my lead. I just want to share how I manage my portfolio monthly with all the good and the bad. I hope you can learn from my experience.

Big Beautiful Bill?

Since Trump won the election in November, the media did a fantastic job at creating as much noise as possible. To be clear, I include all classic media, as well as podcasts, blogs, YouTube, and other “finfluencers” across the board. I get it – noise and fear create a lot of views and clicks, and many make a living out of it.

But any topic starting with “could, would, should, potentially, may, etc” should be considered as market noise and be dumped in the trash. Do you know why? Because you can spend your entire life working on different possible scenarios.

In the end, none of the scenarios you spent hours on will actually happen as you thought they would.

Therefore, there is no point in preparing your portfolio for the new Big Beautiful Bill, just as there is no point in preparing your home for a Chinese invasion. Both are possible, but we are not there yet. But I’m a good player and I’ll tell you more about the Bill and why you should not lose sleep over it yet.

First, let’s review my portfolio.

Performance in Review

Let’s start with the numbers as of June 5th, 2025:

Original amount invested in September 2017 (no additional capital added): $108,760.02.

- Current portfolio value: $295,593.90

- Dividends paid: $5,184.57 (TTM)

- Average yield: 1.75%

- 2024 performance: +26.00%

- VFV.TO= +35.24%, XIU.TO = +20.72%

- Dividend growth: +12.22%

Total return since inception (Sep 2017 – June 2025): 171.79%

Annualized return (since September 2017 – 91 months): 14.09%

Vanguard S&P 500 Index ETF (VFV.TO) annualized return (since Sept 2017): 15.36% (total return 195.60%)

iShares S&P/TSX 60 ETF (XIU.TO) annualized return (since Sept 2017): 11.19% (total return 123.60%)

Big Beautiful (Bill) Noise, Same Strategy

What’s the Big Beautiful Bill

The Big Beautiful Bill, which I’ll refer to as BBB for simplicity’s sake, is a 1,000-page bill including tons of reforms. It was recently passed by the House of Representatives (led by Republicans) in May. The bill is currently under consideration in the Senate. Senate Republicans are working towards finalizing the bill, aiming for a vote before the July 4th recess.

As you might imagine, it encompasses a wide range of things. What caught Canadians’ interest is Section 899, which proposes to override existing tax treaties and introduce a punitive tax regime for countries the U.S. deems to have “unfair” tax practices.

Canada is in the Bill’s score thanks to its digital service tax. Therefore, many experts expect Canada to be punished according to Section 899. Under this provision, the withholding tax on U.S. dividends for Canadian investors could increase by 5% annually, reaching up to 50% over several years.

What makes many freak out is that it could also override the current Canada-U.S. Tax Treaty, including the 0% U.S. withholding tax on dividends received within registered retirement accounts such as RRSPs or RRIFs.

In other words, all U.S. dividends could be subject to extra taxes.

Why it doesn’t matter

I understand that such news spreads fast and creates chaos. But it doesn’t matter: the bill is not a law yet.

Many asked me why I have not actively covered tariffs’ news over the past 6 months. I think you have your answer now: noise, noise and more noise. So far, very little has been done on that front and more confusion is to come. I’ll look seriously at tariffs once they are applied and officially there to stay. That could take another 6 months or possibly even longer!

Back to the BBB where we are currently in the “what if” world. Nothing is officially signed or approved to become law. In fact, the bill faces challenges due to concerns over its projected impact on the federal deficit and proposed cuts to Medicaid.

The Senate is expected to propose amendments to address these concerns, particularly focusing on fiscal savings and adjustments to Medicaid provisions. Once the Senate passes its version, the bill will return to the House for reconciliation of any differences. If both chambers agree on the final text, the bill will be presented to President Trump for his signature.

Then, and only then, it might be judicious to start worrying. On second thought, you really should not worry at all. Here’s what you should be doing if you are inclined to worry.

What should you do

The best thing to do when changes threaten your investment is to know your current position. For example, you can calculate how much U.S. dividends you receive. I did the exercise for all my portfolios, and I get about $2K from U.S. companies (that’s one advantage of a low-yield, high-growth approach). If the bill is passed, I can take plenty of time to calculate the impact on my portfolio return, as the bill expects to raise the tax by 5% per year. It is not going to 50% the day after it passes.

Then, once you know where you stand, you can also consult a tax expert. Be warned that the chances are that the tax expert will tell you what you just read in this newsletter: There is not much to do at this point since nothing has been passed. Finally, you should enjoy summer and wait until you get news that the bill has become law.

Smith Manoeuvre Update

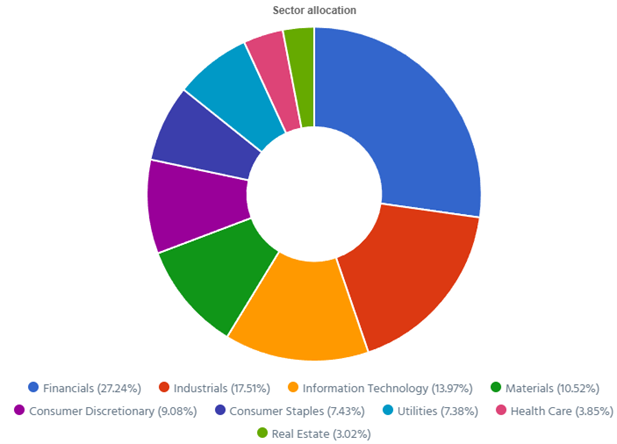

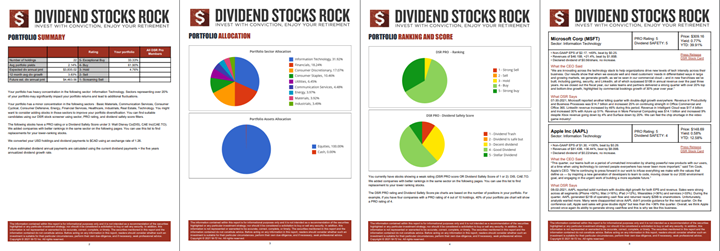

Slowly but surely, the portfolio is taking shape with 13 companies spread across 8 sectors. My goal is to build a portfolio of thriving companies with a solid dividend triangle (e.g. with positive revenue, EPS and dividend growth trends). The current portfolio yield is at 3.17% with a 5-year CAGR dividend growth rate of 11.07%.

The portfolio value is now at $20,772.47.

The portfolio debt is at $17,500.

The annual income is $658.24.

To report my Smith Manoeuvre, I export the Excel data from my DSR PRO dashboard.

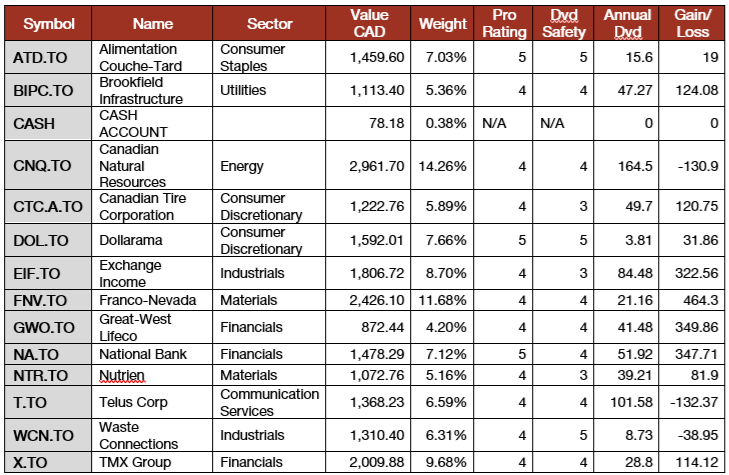

Smith Manoeuvre Portfolio Summary

Here’s my SM portfolio summary as of June 5th 2025 before markets open:

Adding more of Dollarama (DOL.TO)

After adding Dollarama to my portfolio last month, I just bought 4 more shares with my latest SM contribution ($750). With this new purchase, DOL is now 7.66% of the portfolio, ranked 5th in weight.

As we don’t know what will happen with tariffs and the Canadian economy, I’m increasing my position in a recession-resistant company. There is nothing like buying a defensive stock that can also grow by double digits.

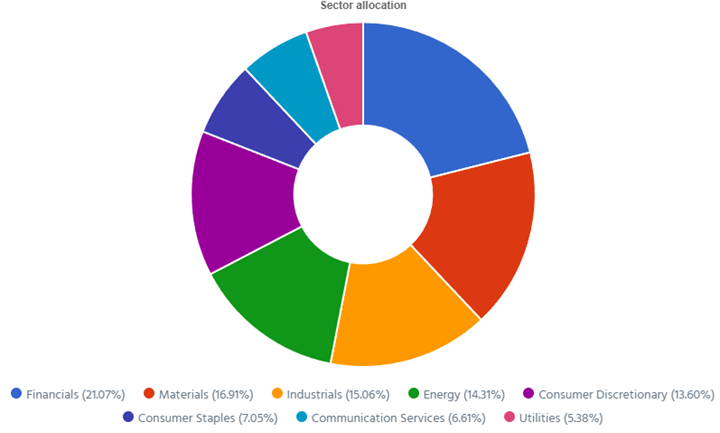

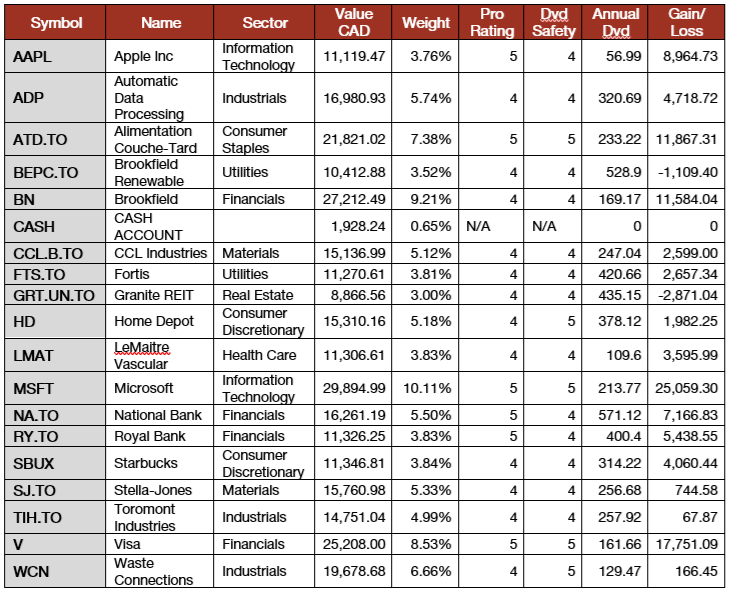

Pension Portfolio Summary

Here’s my pension plan portfolio summary as of June 5th 2025 before markets open:

Total value: $295,593.90 (+ $14,104.75 or +5% from last month).

Many Canadian companies reported their earnings in the past few weeks. Let’s start the round-up!

Brookfield keeps growing its assets under management

Brookfield Corporation reported a solid quarter with distributable earnings (DE) per share up 27%. Results by segments were as follows: Asset Management had DE of $684M supported by record fee-related earnings of $698M, which was up 26%, fueled by $25B in capital inflows and a 20% rise in fee-bearing capital to $549 billion. Wealth Solutions had DE of $430M, benefiting from $4B in annuity sales and an increase in insurance assets to $133B. Operating Businesses generated DE of $426M, with notable contributions from renewable power, infrastructure, private equity, and real estate, including 3% growth in same-store net operating income. During the quarter, BN bought back $850M of its shares.

In case you wonder which one is best between BN and BAM, I have discussed them in this 10-min episode:

CCL Industries packages profit

CLL Industries reported a great quarter with revenue and EPS up 9%. This growth was driven by 3.8% organic growth. 1.4% of that growth came from acquisitions, and a 3.4% positive impact from foreign currency translation. The CCL segment achieved 4.5% organic sales growth, propelled by strong demand in Home & Personal Care, especially aluminum containers in the Americas, and robust label sales in Europe and Mexico. The Innovia segment also delivered strong results, while the Checkpoint segment faced restructuring costs of $0.8 million related to severance. CCL also announced a share buyback program of up to 8.82% of issued capital.

Fortis powers steady growth

Fortis reported a solid quarter with earnings up by 7.5%. This growth was primarily driven by rate base expansion across its regulated utilities, most notably at Central Hudson, which benefited from the conclusion of its 2024 general rate application. Favorable foreign exchange rates also contributed positively. However, these gains were partially offset by higher holding company financing costs, lower margins on wholesale sales in Arizona, and the expiration of a regulatory incentive at FortisAlberta. Fortis invested $1.4 billion in capital expenditures during Q1 2025, aligning with its $5.2 billion annual capital plan.

Granite REIT can’t get the market to love industrial properties (despite great numbers)

Granite REIT reported a solid quarter with revenue up 11% and AFFO per unit up 16%. This brings the AFFO payout ratio down to 60%. Net operating income (NOI) rose to $125.7 million, up from $114.5 million, driven by contractual rent adjustments, CPI-linked increases, and the commencement of leases on four development and expansion projects in Canada, the U.S., and the Netherlands. Same property NOI (cash basis) increased 4.7% in constant currency terms. The REIT maintained 94.8% occupancy, slightly down from 94.9% at the end of 2024. GRT maintained its 2025 guidance from February 2025, forecasting FFO per unit of $5.70–$5.85 and AFFO per unit of $4.80–$4.95.

Home Depot’s renovation projects shrink

Home Depot reported a mixed quarter with revenue up 9%, but EPS declined by 2%. Despite the overall revenue growth, comparable sales declined by 0.3%, with U.S. comparable sales showing a modest 0.2% increase. The revenue boost was primarily driven by a 2.1% increase in customer transactions, while the average ticket size remained flat. This suggests that while more customers are shopping, they are spending similar amounts per visit, indicating a focus on smaller-scale projects. The decline in earnings was attributed to a shift in consumer spending towards smaller projects and a slowdown in large-scale home improvement activities.

Did I ever tell you I love National Bank?

National Bank reported another strong quarter with revenue up 33% and adjusted EPS up 12%. The revenue growth came from the Canadian Western Bank acquisition. PCLs also jumped from $138M to $545M, driven by an additional $230M coming from CWB. Personal & Commercial net income was up 2%. Wealth Management was up 13%, driven by fee-based revenues. Financial Markets increased by 56%, driven by growth in global markets’ revenues. U.S. & International was up 4% with higher revenue, but was offset by higher PCLs. The bank increased its dividend by 3.5%. The quarter’s story was the CWB acquisition for $6.8B which significantly bolsters National Bank’s national presence and product reach.

I have reviewed all Canadian Banks’ most recent earnings below:

Royal Bank’s acquisition bolsters results

Royal Bank reported a solid quarter with revenue up 11% and EPS up 7%. Personal Banking was up 14%, driven by the HSBC acquisition and by higher net interest income reflecting higher spreads and average volume growth of 7% in deposits and 4% in loans. Commercial Banking improved by 3%, supported by the HSBC acquisition, but hurt by higher PCLs. Wealth Management was up 11% on higher fee-based assets. Insurance was up 19% on higher insurance service results. Capital Markets were down by 5% and were affected by higher non-interest expenses and higher taxes . The Bank also raised its dividend by 4% and announced a share buyback program for up to 35 million shares.

Stella-Jones is stalling

Stella-Jones reported a mixed quarter, with sales remaining flat, but EPS increased by 23%. Revenue was impacted by a $38M currency conversion effect. Segment-wise, utility poles were up 4%, largely due to favorable pricing despite slightly lower volumes. Railway ties were off 8% due to a Class 1 railroad shifting to internal production and delayed project timing. Residential lumber was stable, and industrial products were up 8%. Logs and lumber were off 17% due to less trading activity. The boost in EPS and margins was primarily driven by a one-time insurance gain and operational cost discipline, amid stable revenue.

I have shared my complete SJ.TO stock analysis on the Moose Markets.

A Business Built Around Utility Poles and Railway Ties — And It Works

Now I’m only waiting for Alimentation Couche-Tard to report its earnings to wrap this quarter!

My Entire Portfolio Updated for Q1 2025

Each quarter, we run an exclusive report for Dividend Stocks Rock (DSR) members who subscribe to our special additional service, DSR PRO.

The PRO report includes a summary of each company’s earnings report for the period. I wanted to share my own DSR PRO report for this portfolio.

You can download the full PDF, which contains all the information about my holdings. Results have been updated as of April 2nd, 2025.

Download my portfolio Q1 2025 report.

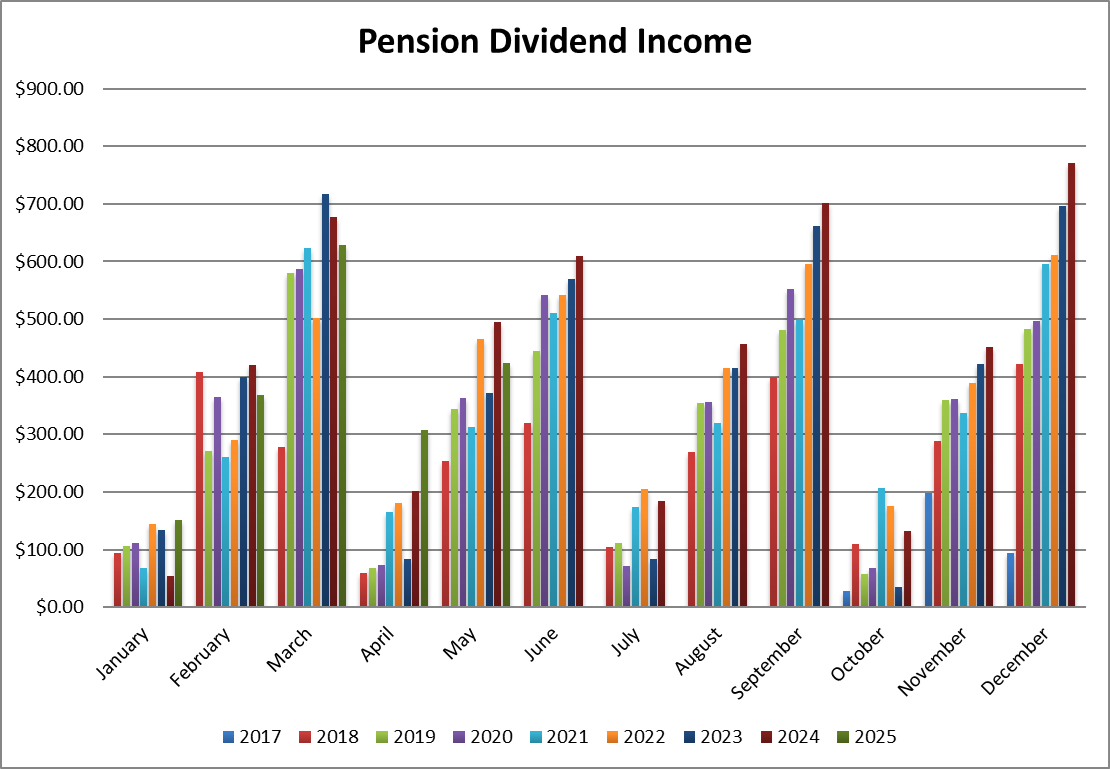

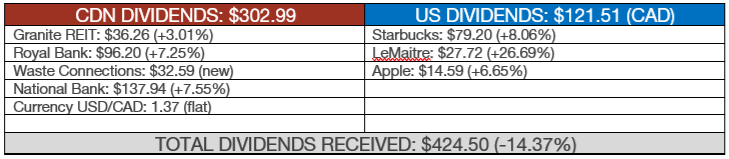

Dividend Income: $424.50 (-14.37% vs May 2024)

I’ve received a bit less this month as I sold my shares of Texas Instruments ($65 USD in dividends last year) and Magna International ($44.81). My new position at Waste Connections partially offsets the loss. All other companies paid me more this year compared to last year, as most of them reported high single-digit increases.

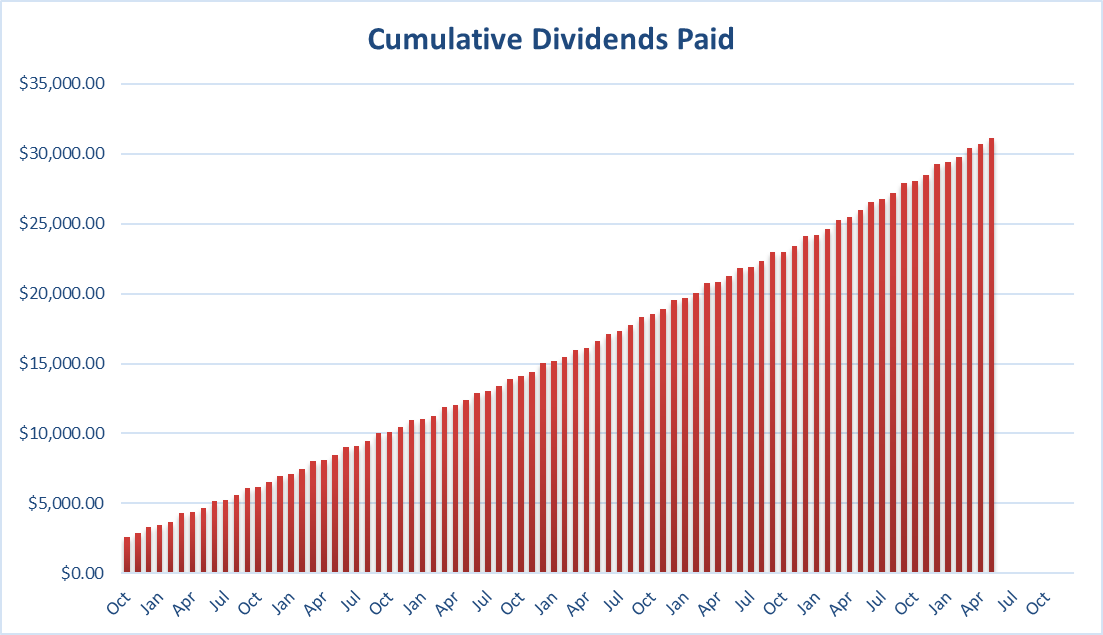

Since I started this portfolio in September 2017, I have received a total of $31,145.39 CAD in dividends. Keep in mind that this is a “pure dividend growth portfolio” as no capital can be added to this account other than retained and/or reinvested dividends. Therefore, all dividend growth is coming from the stocks and not from any additional capital being added to the account.

Final Thoughts

I’m letting the dividends pile up a bit in my portfolio right now. I have almost $2,000 in cash, which is not even 1% of the portfolio. I will likely use it to invest in my smallest positions. The candidates are Granite, Brookfield Renewable, and Starbucks at this point.

Next month, I’ll have enough to buy something. It’s great to see this dividend snowball growing!

Cheers,

Mike.

Leave a Reply