In 2016, I made a life-changing decision: I took a sabbatical, put my family in a small RV, and drove to Costa Rica.

Upon my return in 2017, I officially quit my job as a private banker at National Bank and started working full-time on my baby: Dividend Stocks Rock. I also decided to manage my pension account held at the National Bank. I’ve built this portfolio publicly since 2017 to make a real-life case study. I decided to invest 100% of this money in dividend growth stocks.

In August 2017, I received $108,760.02 in a locked retirement account. This means I can’t add capital to the account, and growth is only generated through capital gains and dividends. I don’t report this portfolio’s results to brag about my returns or to tell you to follow my lead. I just want to share how I manage my portfolio monthly with all the good and the bad. I hope you can learn from my experience.

All that fuss…

When I wrote my last update, I had numbers as of April 2nd before the stock markets open. I guess it was a good thing since the market got destroyed by Trump’s announcements by the end of that week. We started to see headlines about bear markets and stagflation (I can’t believe people keep talking about something that happened once… 50 years ago!).

Only 4 tiny weeks later, I’m reporting on my portfolio to see that I’ve lost a massive, gigantic, enormous… TWO PERCENT???

Let’s discuss volatility. But first, here are the results!

Performance in Review

Let’s start with the numbers as of May 1st, 2025 (before the bell):

Original amount invested in September 2017 (no additional capital added): $108,760.02.

- Current portfolio value: $281,489.15

- Dividends paid: $5,207.95 (TTM)

- Average yield: 1.85%

- 2024 performance: +26.00%

- VFV.TO= +35.24%, XIU.TO = +20.72%

- Dividend growth: +12.22%

Total return since inception (Sep 2017 – April 2025): 158.82%

Annualized return (since September 2017 – 90 months): 13.52%

Vanguard S&P 500 Index ETF (VFV.TO) annualized return (since Sept 2017): 14.72% (total return 180.10%)

iShares S&P/TSX 60 ETF (XIU.TO) annualized return (since Sept 2017): 10.52% (total return 111.80%)

All That Fuss for a 2% Decline?

When I wrote my last update, I had numbers as of April 2nd before the stock markets open. I guess it was a good thing since the market got destroyed by Trump’s announcements by the end of that week. We started to see headlines about bear markets and stagflation (I can’t believe people keep talking about something that happened once… 50 years ago!).

Only 4 tiny weeks later, I’m reporting on my portfolio to see that I’ve lost a massive, gigantic, enormous… TWO PERCENT???

I don’t understand as the headlines have tried to sell me a bear market. By definition, a bear market is at least a 20% loss of value. 30 days later, I’m down 2%? Since the beginning of the year, my portfolio is down by less than 7%. It’s not great, but it’s not what has been sold to the public.

So why do so many people think it’s a lot worse than it is?

Volatility

I haven’t looked back for stats, but I can tell April was a crazy month in terms of ups and downs. Violent market swings led investors to think it was a really bad month.

To be clear, April wasn’t great.

What’s coming next may or may not be worse. But in the meantime, volatility created a lot of smoke.

Here’s the killer question: Why is there so much volatility?

I have the beginnings of an answer.

No information is better than changing information

One thing that certainly has not helped since the Trump administration has been in place is the ever-changing information. I’ve been hearing the word “Tariffs” since Trump was elected in November 2024. To this date, it’s still unclear how much tariffs will be applied to what and for how long.

We certainly received information. But the problem is that any piece of information has a hard time surviving 48 hours before being altered or canceled.

The stock market is driven by projections. Financial firms, analysts, investors are making projections for revenue, earnings, cash flow for thousands of companies. But how can you make projections when the information keeps changing?

If my wife tells me she loves me more than anything on Monday, only to wake up on Tuesday with her telling me I should leave, maybe I will not be willing to get into a big project like buying a house or having a kid with that “crazy lady”. I’ll wait until I get a clearer picture of us as a couple before making any firm projections.

The same goes for the stock market.

Hedge funds & leverage

Since the financial crisis of 2008, hedge funds and the use of leverage have amplified volatility. Since then, many financial firms have used heavy leverage to generate strong returns in the market. Leverage is great as long as the market goes up. When it goes down, the losses are also amplified.

When the market is volatile, investors may face margin calls. That happens when a leveraged portfolio value goes down too low and reaches a limit set by the banker. The banker then calls the investor and asks for more capital to maintain the portfolio above the limit. If the investor can’t add capital, all positions are sold immediately.

You can imagine how fast it can push the market when it happens to major financial firms. Plus, there is a chance of a domino effect.

The dividend is still good and increasing

In the meantime, my ultimate trick remains the same: I don’t bother looking at my portfolio values. I prefer looking at my dividend growth rate. While my portfolio value declined since the beginning of the year, my dividend payments have increased.

This tells me investors are spooked by volatility, but most companies I hold are doing great and generating more revenue, more earnings, and more cash flow. Therefore, I have nothing else I need to do with my portfolio!

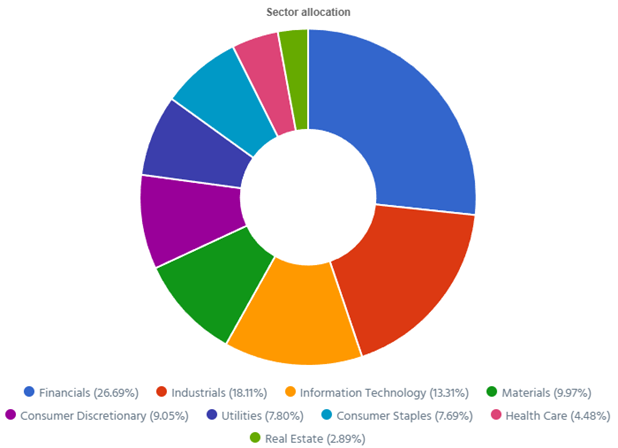

Smith Manoeuvre Update

Slowly but surely, the portfolio is taking shape with 13 companies spread across 8 sectors. My goal is to build a portfolio of thriving companies with a solid dividend triangle (e.g. with positive revenue, EPS and dividend growth trends). The current portfolio yield is at 3.44% with a 5-year CAGR dividend growth rate of 11.08%.

New Reporting Style – Same Portfolios

This is just a quick note to tell you that I will report my portfolios differently going forward.

I used to log into my brokerage account and manually enter each position in this recap. Then, I realized I could export the Excel data from my DSR PRO dashboard and save a lot of time!

I’m also adding the ratings, the expected annual dividend and the gain or loss in dollars for each position.

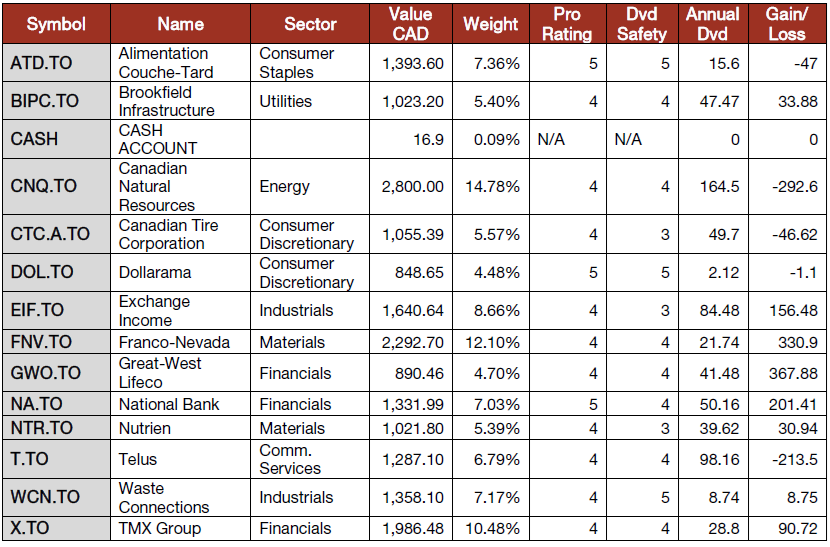

Smith Manoeuvre Portfolio Summary

Here’s my SM portfolio summary as of May 2nd 2025 before markets open:

Adding Dollarama (DOL.TO)

I had about $100 in the cash account, plus another $750 from my monthly contribution to invest in Dollarama. I regret not adding this one to my portfolio sooner, so better now than never!

DOL runs compact stores (avg. 8,500 sq ft) in high-traffic areas across Canada. Over 90% of its revenue comes from general merchandise and consumables with 60% from private-label goods. It executes a fixed-price strategy (now up to $5), enabling cost controls and consistent shopper expectations. The company can grow by opening new stores and through its expansion in Central America (Dollar City). It has also made an offer to acquire the Reject Shop in Australia.

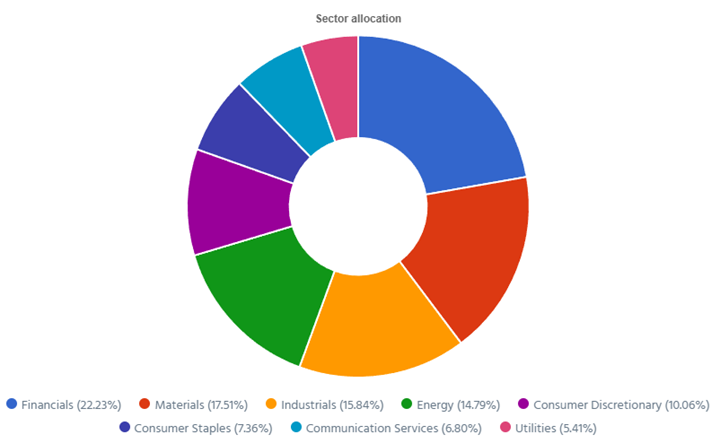

Pension Portfolio Summary

Here’s my pension plan portfolio summary as of May 2nd 2025 before markets open:

Total value: $281,489.15 (down $6,049.46 or -2.10% from last month).

Many companies reported their earnings in the past few weeks. Let’s start the round-up!

Apple’s results are driven by its Services segment

Apple reported a good quarter with revenue up 5% and EPS up 8% which beat the analysts’ expectations. The growth was primarily driven by strong performance in the Services segment which achieved a record $26.65B in revenue (+12%). iPhone sales rose 2% bolstered by the launch of the iPhone 16e. Mac and iPad revenues increased by 7% and 15%, respectively. However, the Wearables, Home, and Accessories segment experienced a 5% decline, indicating potential market saturation or increased competition in that category. The EPS improvement reflects Apple’s ability to manage costs effectively and leverage its high-margin Services business.

Automatic Data Processing is printing money

Automatic Data Processing reported another good quarter with revenue and EPS up 6% which beat the analysts’ expectations. Revenue grew 6% on an organic constant currency basis. Employer Services contribution was up 5% year-over-year supported by a 1% increase in U.S. pays per control. PEO Services delivered stronger growth by rising 7% or 8% excluding zero-margin benefits pass-throughs. The increase in PEO was driven by a 2% rise in average paid worksite employees reaching approximately 748,000. The company also reported an 11% increase in interest on funds stemming from a 7% increase in average client fund balances and a 10-basis point increase in yield to 3.2%.

Brookfield Renewable keeps on chugging

Brookfield Renewable reported a good quarter with revenue up 6% and FFO per share up 7%. This growth was driven by the commissioning of new capacity and recent acquisitions including the privatization of Neoen and the agreement to acquire National Grid Renewables. The hydroelectric segment generated $163M in Funds from Operations (FFO) with generation in line with long-term averages. Wind and solar segments contributed $149M in FFO, benefiting from newly commissioned capacity and recent acquisitions. The distributed energy, storage, and sustainable solutions segments performed well by generating a combined $126M in FFO which was double from the prior year.

LeMaitre Vascular is healthy but it’s not enough for investors

LeMaitre Vascular reported a good quarter with revenue up 12% and EPS up 9%, but it wasn’t enough to please investors. The revenue growth was primarily driven by strong demand for grafts which saw a 17% increase, and carotid shunts which were up 14%. Geographically, the Europe, Middle East, and Africa (EMEA) regions led with an 18% sales increase, followed by the Americas at 11%, and Asia-Pacific at 3%. The company’s direct-to-hospital sales model continues to provide a competitive edge in the niche medical device market. The gross margin improved by 60 basis points to 69.2% which was attributed to higher average selling prices coupled with manufacturing efficiencies.

Did I ever tell you that Microsoft is a beast?

Microsoft reported another strong quarter with revenue up 13% and EPS up 18% which easily beat the analysts’ expectations. This growth was primarily driven by the Intelligent Cloud segment (+21%) with Azure and other cloud services growing 33%. The Productivity and Business Processes segment was up 10%, bolstered by Microsoft 365 and Dynamics 365. The More Personal Computing segment saw revenue go up by 6%, with notable growth in Xbox content and services (up 8%) and search and news advertising revenue (up 21%). Capital expenditures totaled $21.4B, which was slightly lower than expected with approximately half allocated to long-lived assets supporting AI and cloud services.

Starbucks coffee is still sour

Starbucks reported a weak quarter with revenue up only 2%, but EPS dropped by 40%. The decline in EPS was primarily due to increased costs associated with the “Back to Starbucks” initiative which included higher labor expenses and restructuring costs. The North American segment was up 1% driven by a 5% growth in company-operated stores. However, comparable store sales declined by 1% primarily due to a 4% decrease in transactions that were partially offset by a 3% increase in average ticket size. The international segment sales were up 6%. China’s comparable store sales were flat which ended a streak of four consecutive quarters of decline.

I have shared a complete stock analysis of the coffee shop here.

Brewed for Loyalty, Facing the Heat: This One is Under Pressure

Toromont Industries margin struggles

Toromont reported a mixed quarter with revenue up 7%, but EPS fell by 10%. The Equipment Group was up 7% with new equipment sales up 24% due to strong deliveries in mining and power systems. Rental activity also rose by 11%. However, used equipment sales declined by 21%, and product support revenues decreased by 3%, reflecting cautious customer demand. CIMCO’s revenue increased by 9% and was supported by a 15% rise in package revenue and a 5% increase in product support activity. ?The decrease in profitability was attributed to lower gross margins in the Equipment Group due to an unfavorable sales mix and slightly higher expenses.

Visa is… perfect?

Visa reported another solid quarter with revenue up 9% and EPS up 10% which easily beat the analysts’ expectations. This growth was driven by strong increases in key business drivers: payments volume grew 8%, total cross-border volume rose 13%, and processed transactions increased 9%. Segment revenues included service revenue of $4.4B (+9%), data processing revenue of $4.7B (+10%), and international transaction revenue of $3.3B (+10%). Other revenue grew significantly by 24% to $937M. Client incentives, which are recorded as a reduction to revenue, increased 15% to $3.7B. Visa’s board authorized a new $30B multi-year share repurchase program.

Waste Connections

Waste Connections reported another solid quarter with revenue up 8% and EPS up 9% and beat the analysts’ expectations. This growth was primarily driven by a 6.9% increase in core pricing with contributions from recent acquisitions totaling $112 million. The Eastern region led with a 12% revenue increase, followed by the Southern region at 8%, and Canada at 8%. Solid waste volumes declined by 2.8% which was attributed to weather-related impacts and the strategic shedding of lower-quality contracts. Landfill tons increased by 1%, with special waste tons up 6% that was partially offset by a 6% decrease in construction and demolition (C&D) tons.

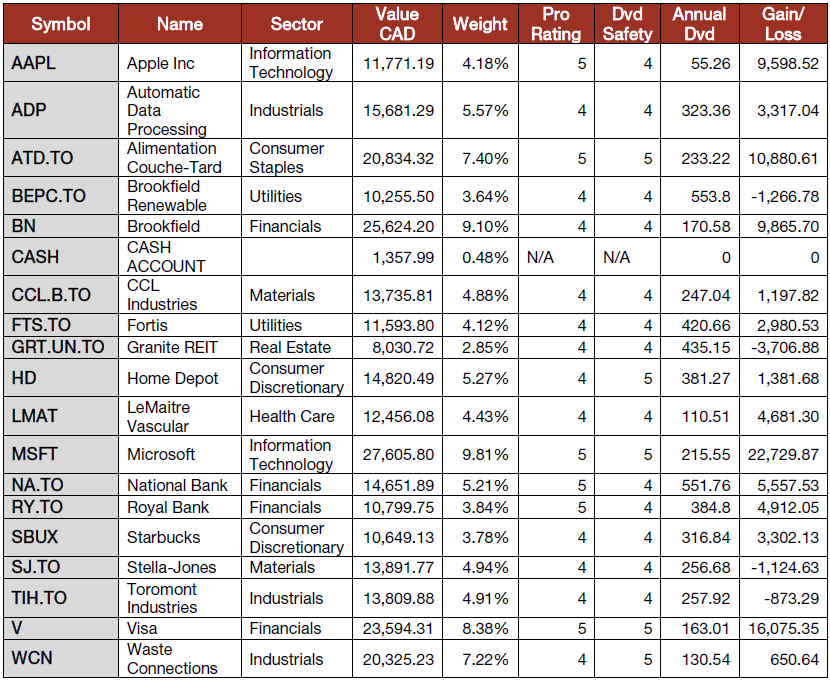

My Entire Portfolio Updated for Q1 2025

Each quarter, we run an exclusive report for Dividend Stocks Rock (DSR) members who subscribe to our special additional service, DSR PRO.

The PRO report includes a summary of each company’s earnings report for the period. I wanted to share my own DSR PRO report for this portfolio.

You can download the full PDF showing all the information about all my holdings. Results have been updated as of April 2nd, 2025.

Download my portfolio Q1 2025 report.

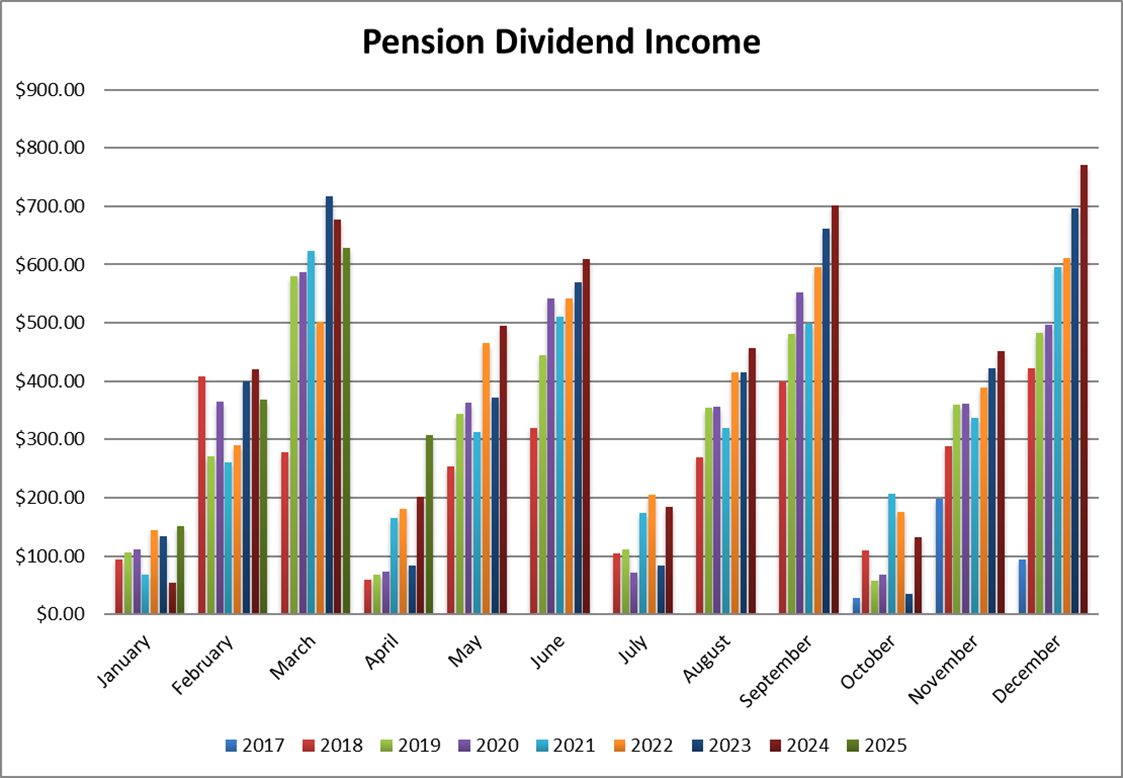

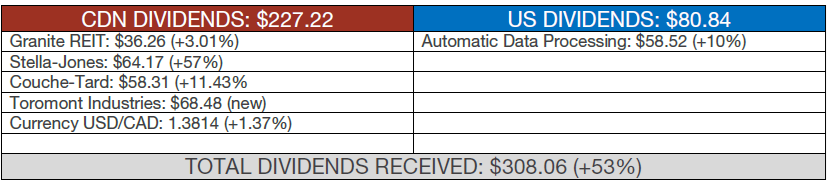

Dividend Income: $308.06 (+53% vs April 2024)

I’m getting more dividends for this month mostly driven by the addition of Toromont Industries and a full position in Stella-Jones. Special mention to Couche-Tard and Automatic Data Processing for the double-digit increase vs. last year!

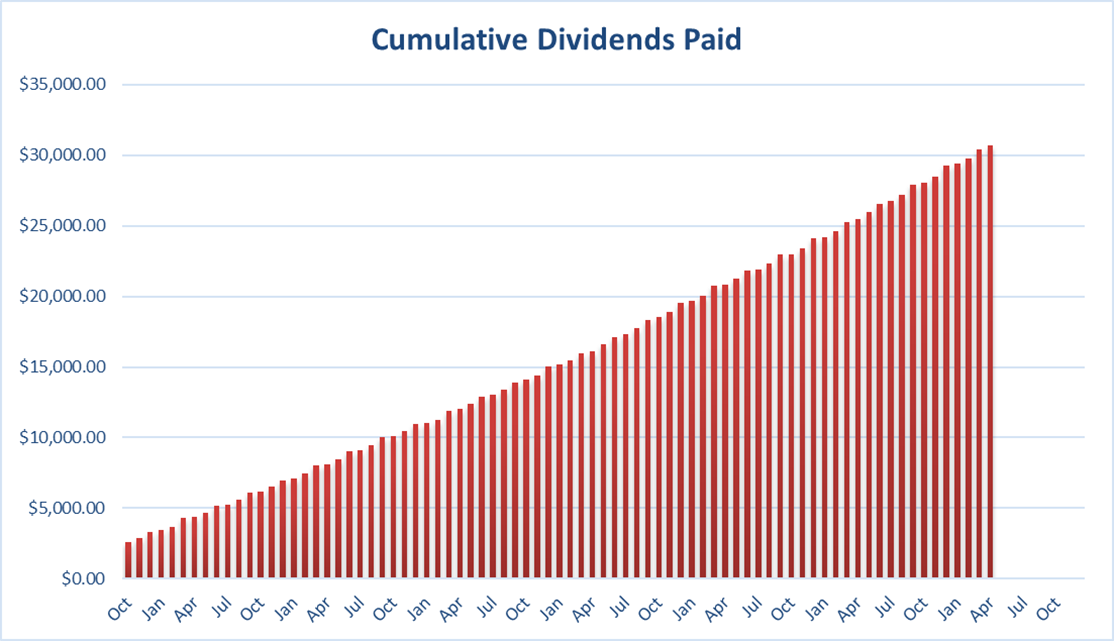

Since I started this portfolio in September 2017, I have received a total of $30,720.89 CAD in dividends. Keep in mind that this is a “pure dividend growth portfolio” as no capital can be added to this account other than retained and/or reinvested dividends. Therefore, all dividend growth is coming from the stocks and not from any additional capital being added to the account.

Final Thoughts

I’m letting the dividends pile up a bit in my portfolio right now. I have a little over $1,300 in cash. I will likely use it to invest in my smallest positions. The candidates are Granite, Brookfield Renewable and Starbucks at this point.

The next two months are big dividend months. I’ll likely wait until I reach $2K before using my capital. It’s great to see this dividend snowball continuing to grow!

Cheers,

Mike.

Leave a Reply