Since January, the market has paid up for a short list of winners and walked past a lot of good businesses. That gap is where I went looking this week.

Both stocks in this piece came off the same screen: a DSR PRO rating of at least 4, a Dividend Safety score of at least 4, and a price under 21 times earnings. In a market where almost everything looks expensive, buying a quality business for less than 20 times earnings feels rare.

One is an American defense giant that fell 35% this year. The other is a Canadian packaging company most people have never heard of. Different countries, different sectors, same reason they caught my eye. The price moved down while the business kept moving forward.

Disclosure: I own CCL Industries. I do not own Northrop Grumman. This is education, not advice. Do your own due diligence.

What value means on this buy list

A cheap stock and a good value are not the same thing. A falling price on a broken business is a trap. A falling price on a healthy business is an invitation to look closer.

So we start with the dividend triangle: revenue, earnings, and dividend growth over five years. Then we check whether the dividend is safe, whether the balance sheet can carry the company through a rough patch, and how today’s valuation compares to the stock’s own history. Not the market’s average. Its own record.

When a stock trades below its usual multiple and the three lines of the dividend triangle still point up, the discount is worth a closer look. Both names below fit that description, in very different ways.

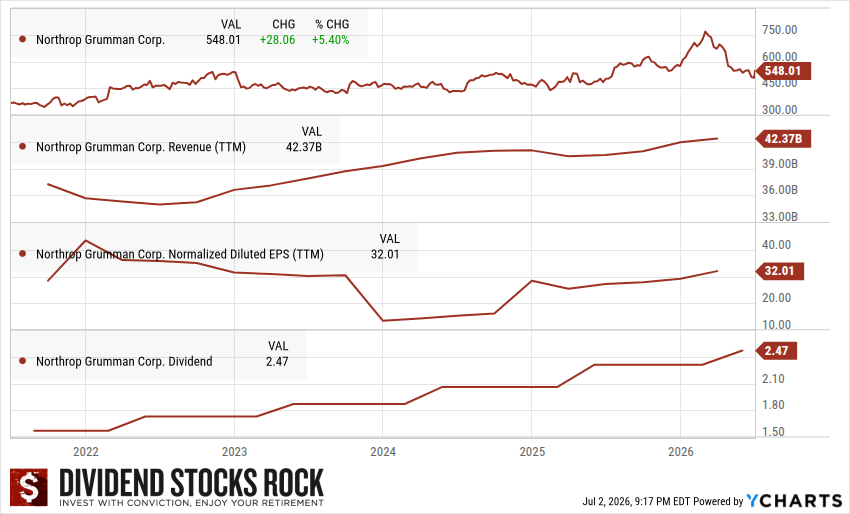

Northrop Grumman (NOC): Beaten Down, Not Broken

Investment thesis: Northrop is a leading defense-technology contractor with key roles in the B-21 bomber and F-35 programs and a lock on high-altitude, long-endurance drones. About 95% of sales come from government contracts, and the backlog sits near a record $96B, which gives years of revenue visibility. Rising defense budgets across the US and its allies keep demand climbing. The dividend triangle is uneven, but the dividend itself has grown close to 10% a year for five years.

Here is the tension. Revenue grew 2.4% a year over five years and earnings 2.9%, yet the dividend climbed 9.7%. That gap is why the payout ratio matters. Right now it sits near 31%, with a cash payout ratio near 40%, so there is plenty of room to keep raising. The latest hike was a strong 12%, to $2.31 per share, and the dividend growth streak now runs 23 years.

The story this year is the price. NOC fell from about $768 to roughly $499, a drop near 35%, even as the backlog hit that record $96B. The decline came from margin worries on the B-21, where cost-plus contracts carry lower profitability, plus a wave of analyst target cuts across the sector. The thesis did not break. Expectations got ahead of the stock, the company gave conservative guidance, and shares fell after earnings.

That is the classic setup. Decent numbers, a stock that drops because the market wanted more.

The valuation now tells the value story. NOC trades around 16 to 17 times earnings against a 5-year average near 19. The forward yield is close to 2%, above its 5-year average near 1.6%, another sign the price has fallen relative to the business. The question for your research is whether you trust management to hit its 2026 margin and EPS targets. That is what turns the discount into a return.

What to watch: B-21 production progress and any margin update, since that is the swing factor. New defense awards and the backlog trend. Free cash flow against the $3.1B to $3.5B target for 2026. The next earnings date is July 21, 2026.

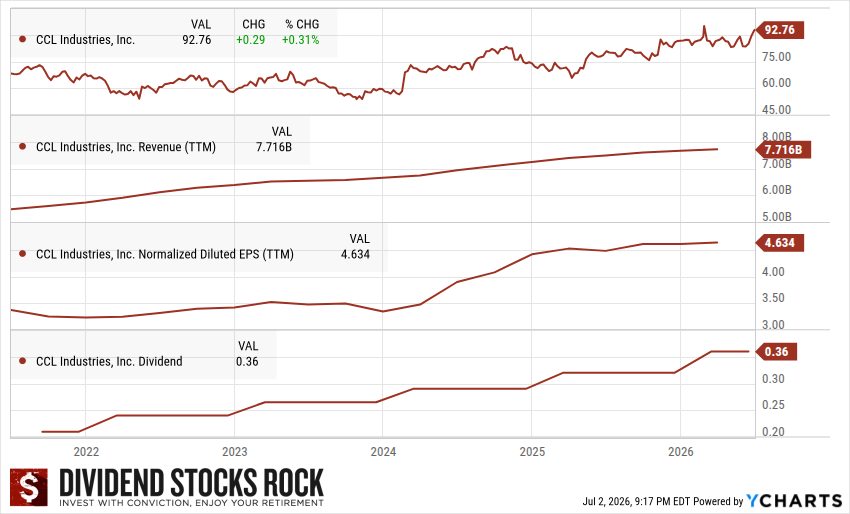

CCL Industries (CCL.B.TO): The Boring Compounder

Investment thesis: CCL is a global leader in specialty labels and packaging, serving consumer goods, healthcare, automotive, and technology through four segments. It grows low single digits organically and bolts on smart acquisitions, from Avery in 2013 to Checkpoint, Innovia, and the pending Sleever deal. A diversified product line, a global footprint, and steady cash flow make it a stable long-term holding. The dividend triangle is close to perfect.

This is the opposite profile from Northrop. Revenue grew 7.1% a year over five years, earnings 6.5%, and the dividend 11.75%. All three lines point up and stay close together, which is exactly what you want to see. The Lang family holds a controlling stake, so management runs the business like owners.

The dividend is well protected. The payout ratio sits near 28% and the cash payout ratio near 27%, among the lowest on the buy list. After a smaller bump in 2020, CCL delivered double-digit raises almost every year since. The 2026 increase was 12.5%, to $0.36 per share, and the streak now stands at 24 years.

CCL is the steady name here, up about 18% over the past year, so this is less about a crash and more about valuation discipline. The stock trades near 17 to 18 times forward earnings against a 5-year average close to 19, so you are paying near fair value, not grabbing a deep discount. The live risk is margins. Aluminum, resin, and energy costs jumped in early 2026, and an equipment outage at a Pennsylvania plant added pressure. The question is whether CCL can keep its earnings growing while it passes those costs through.

I hold CCL and treat it as a core holding. It is a boring business. Labels and packaging will never trend on social media. They do print reliable cash flow, year after year, and that is the point.

What to watch: the Sleever acquisition close and how fast it contributes. Input-cost inflation in aluminum and resins, and how much CCL can pass on. The Pennsylvania facility’s return to full capacity. The next earnings date is August 11, 2026.

Two flavors of value

These two names show that cheap comes in more than one form.

Northrop is a beaten-down leader. The price fell hard, the multiple compressed below its history, and the payoff depends on management delivering on the B-21. More reward if they do, more risk if they stumble.

CCL is a steady compounder at a fair price. No drama, a near-perfect dividend triangle, and a cost-inflation question to monitor. Less upside from the valuation, more certainty in the business.

Same screen, two very different bets. That is what a buy list is for. A starting point for your own work, not a finish line.

The Hard Part Is Knowing When to Buy

Finding NOC and CCL took one screen and twenty minutes. Knowing when to buy them is the part that trips up most investors. A stock is down 35%. Is that a gift or a warning? A stock is at fair value. Do you wait, or do you start?

That is what I teach in Dividend Simplified. It is a short, practical course that walks through my buy process, my sell process, and how to read a quarterly earnings report without a finance degree. Bite-sized videos, PDF guides, and the same checklists I use. The whole thing costs $15.

If you have ever stared at a stock like Northrop and frozen, this course was built for you.

Thanks for sharing! It was great to stop by and read your latest post about these 2 stocks on your buy list. I’m back after a long blogging hiatus, so it was a pleasant surprise to see a familiar blogger still here. Looking forward to reconnecting and reading more of your work! AFFJ