TFI International is not a stock for investors who panic at the first ugly quarter. When freight volumes drop, earnings fall fast, sentiment turns sour, and the stock can get punished in a hurry. That’s exactly what happened when management warned that profits could fall sharply and the market hit the brakes.

But this is where things get interesting. TFI is still one of the largest transportation and logistics players in North America, with a strong network, proven acquisition playbook, and the kind of scale that can drive serious profitability when the cycle turns. The stock has already absorbed a lot of bad news. Now the real question is whether investors are looking at a broken story or a cyclical reset that could create an opportunity.

A Network Built to Move More Than Freight

TFI International is one of North America’s largest transportation and logistics businesses. It operates across Canada, the United States, and Mexico through three main segments: less-than-truckload, truckload, and logistics.

That mix matters.

Less-than-truckload, or LTL, is where scale can become a serious advantage. Instead of dedicating an entire trailer to one customer, TFI can consolidate smaller shipments, optimize routes, and improve truck utilization. When that network is managed well, margins improve because the same asset can serve multiple customers more efficiently.

Truckload adds exposure to full-load moves, specialized transport, and brokerage activities. Logistics broadens the model even further through freight forwarding, transportation management, and asset-light services. In other words, TFI is not just a trucking company. It is a transportation platform with multiple ways to generate revenue depending on what the market gives it.

That diversification is part of the appeal. When one segment softens, another can help absorb the blow. It doesn’t eliminate cyclicality, but it does make the business more resilient than a pure-play operator with a narrower footprint.

Why the Market Still Cares

Bull case

TFI’s investment thesis starts with scale and execution.

The company has grown into a major North American player, and it has done so by using acquisitions intelligently. The UPS Freight deal in 2021 was the most visible example. TFI took a large asset, integrated it into its existing network, and improved profitability. That’s not easy to do in transportation, where bad acquisitions can become a drag for years.

The business also generates more than 70% of its revenue from the United States, which gives it exposure to the largest freight market on the continent. Its acquisition of Daseke added more depth in flatbed trucking and industrial end markets, which could become a meaningful tailwind when the cycle turns.

This is also a company that knows how to protect cash flow. Even in a weak environment, management emphasized free cash flow, customer service, and operating efficiencies. That’s exactly what I want to hear from a cyclical company going through a slowdown.

Bear case

Now for the reality check: this stock is volatile for a reason.

Transportation is deeply cyclical. When economic activity slows, shipment volumes fall, pricing gets squeezed, and the benefits of scale start to work in reverse. TFI warned investors early in 2025 that EPS could drop by 30% to 35%, and the market punished the stock immediately.

That pain didn’t come out of nowhere. Freight demand weakened, tariff uncertainty created hesitation among shippers, and management itself acknowledged that when businesses don’t know the rules, they often sit on the sidelines. That is bad news for trucking volumes.

There is also execution risk around acquisitions, ongoing exposure to fuel and labor costs, and leadership transition risk with CEO Alain Bédard retiring. This is not a “sleep well at night” utility. You have to accept the bumps if you want exposure to the upside.

300 Stock Ideas With a Positive Dividend Triangle—Get the List Now

I’ve used the Dividend Triangle to build a list of about 300 companies showing positive 5-year trends for revenue, EPS, and dividends.

The Dividend Rock Stars list is updated monthly and is a great starting point if you want to speed up your stock research.

Save yourself a ton of work—enter your name and email below and I’ll send it to you.

What’s Changed Lately

The latest developments confirm two things: business conditions remain soft, but management is still pulling the right levers.

Revenue and EPS both declined by 8% in the latest quarter, reflecting weaker demand across the board. LTL and Logistics were hit the hardest, which fits the broader narrative of muted freight activity and cautious customers. Still, the company finished 2025 with strong free cash flow and continued improving its U.S. LTL operating ratio. That tells me the business is being managed for the next cycle, not just the current quarter.

Here’s what I’m watching most closely:

- Revenue softness was broad-based, with pressure in LTL, Truckload, and Logistics.

- Lower volumes remain the core issue, not a broken business model.

- Acquisitions helped offset part of the slowdown.

- Management raised the dividend by 4%, showing confidence despite the weaker environment.

- Major acquisitions are on pause, with the focus shifting to smaller tuck-in deals.

- Share buybacks are now part of the capital allocation story.

- CEO Alain Bédard is retiring, which adds a new variable for investors to monitor.

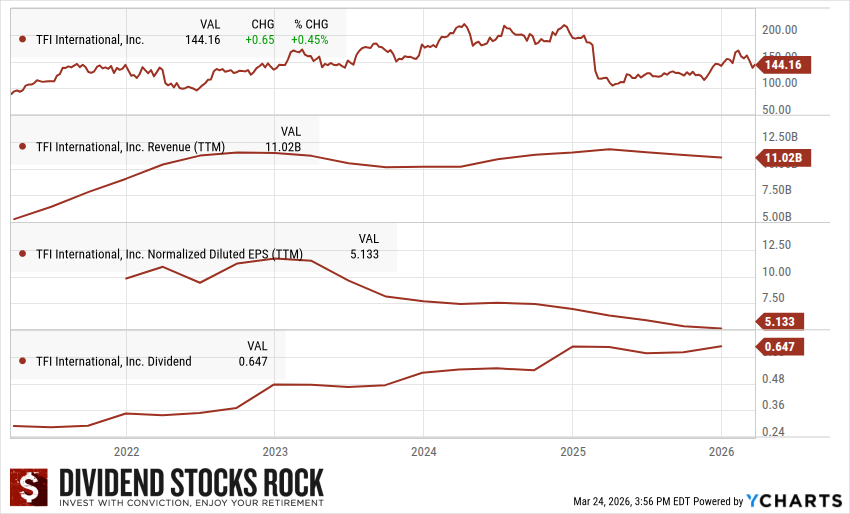

The Dividend Triangle in Action

Revenue climbed strongly through 2022 and then flattened out around the $11B mark. That’s not ideal, but it’s also not a collapse. The bigger issue is earnings. Normalized diluted EPS peaked earlier and has been trending down, landing around 5.13 on a trailing basis. That’s exactly the kind of pattern you expect from a cyclical business under pressure.

The good news is on the dividend side. The payout has continued to move higher and now sits at about 0.647. That fits the thesis that the dividend is still supported by a low payout ratio and solid cash flow.

So, the Triangle is mixed right now. Revenue has stalled, EPS is under pressure, but the dividend keeps rising. That is not the profile of a stock in full breakdown mode. It is the profile of a company going through a cyclical reset while management tries to hold the line.

For dividend growth investors, that distinction is important. I’m not looking for perfection here. I’m looking for signs that the business can endure the downturn and be ready when volumes recover.

A Calculated Bet on the Next Upturn

This is the kind of stock that will make you uncomfortable before it makes you look smart.

TFI International has a proven business model, strong positioning in LTL, a disciplined approach to operations, and a history of extracting value from acquisitions. On the other hand, it remains tied to the freight cycle, tariff uncertainty, and investor sentiment that can turn sour very quickly.

That’s why I see it as an opportunity for investors who understand what they’re buying. Not a core “set it and forget it” holding. Not a low-volatility compounder. But a serious operator that could rebound nicely when freight fundamentals improve.

For the next 12 months, I’d keep my eyes on two numbers above all else: revenue and EPS. If both start to stabilize, the recovery story gets much more interesting.

Want More Stocks That Pass the First Test?

The best opportunities usually start with a simple filter: strong trends in revenue, earnings, and dividends.

That’s exactly what you get with the Dividend Rock Stars list—about 300 companies with a positive Dividend Triangle, updated monthly.

If you want to find more ideas without spending hours screening the market yourself, enter your name and email below and I’ll send it to you.

Leave a Reply