You retire on a Tuesday. The market drops 18% on Wednesday. Same portfolio, same dividend stocks you held last week, and every red number now feels personal.

That gap between feeling and reality is the difference between the accumulation phase and the decumulation phase. When you are 40, a market drop is a sale. When you are 65, it can feel like the end of your retirement plan. The portfolio did not change. Your relationship to it did.

This article walks through what volatility means at each stage, why your age matters less than your conviction, and the practical steps that let you sit through any market drop without flinching.

Short answer: Volatility tolerance has nothing to do with your birthday. It is a function of conviction, cash position, and a written plan. Get those three right and you can hold equities at 75 without losing sleep. Get them wrong and you will panic at 40.

Risk, Hazard, and Volatility Are Not the Same Thing

Most investors mix three concepts together. Untangling them is the foundation of everything else in this article.

Risk is the chance your return differs from what you expected. Every equity investment carries some.

Hazard is any condition that raises the odds of a loss. A penny stock is a hazard. A blue chip with a clean dividend triangle is not. You reduce hazard by avoiding concentration, weak balance sheets, and speculative plays. You cannot eliminate risk.

Volatility tolerance is how much price movement you can stomach before you sell at the wrong time. Investor questionnaires call it risk tolerance. What they measure is volatility tolerance.

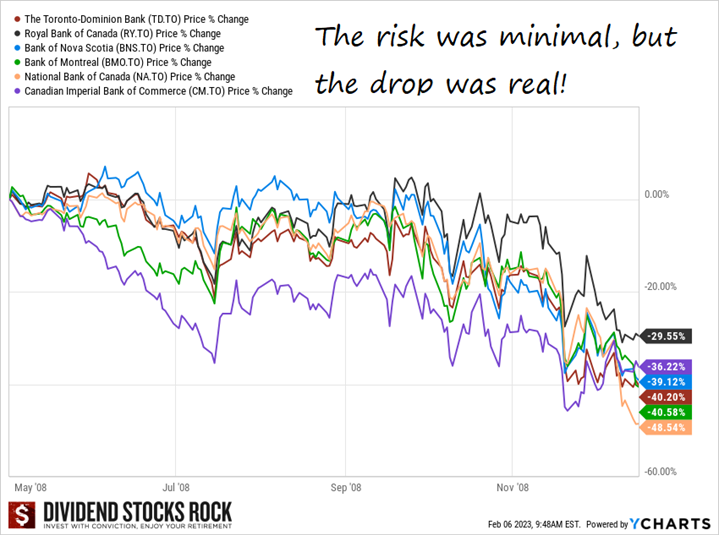

The Canadian banks in 2008 are the textbook case. Their fundamentals were fine. The subprime mess was a US problem. But their share prices dropped 30% to 50% as global markets sold off. Investors who held through the noise recovered their money by the end of 2009, dividends included. The risk was perceived. The volatility was real.

Knowing the difference between price action and business action is the first move toward holding through a downturn.

What Volatility Means at 40

The 2008 crisis hit two groups of investors at the same time. I was in my late twenties. My retired clients were in their seventies. Same crash. Opposite reactions.

When you are still building wealth, volatility works in your favor. Lower prices mean more shares for the same dollar. The math is straightforward. The emotional part is not.

If you contribute every two weeks through a payroll deduction, a 30% drop is the best thing that can happen to a 40-year-old. You buy more units. Your future dividend stream gets a discount. Every bear market you survive while contributing is a gift to your 65-year-old self.

The accumulation phase is also when you learn what kind of investor you are. Not in theory. In practice. How did you feel in March 2020? In 2022? If you sold a position at a loss because the headlines got loud, that is data. It means your allocation is above your true volatility tolerance.

You have two options.

Reduce your equity exposure until you can sleep.

Learn more about the businesses you own so the next drop scares you less.

I prefer option 2. A solar eclipse used to mean the end of the world. Now we put on glasses and watch the show. Knowing how something works changes your reaction to it.

If you struggle with volatility at 40, it will be worse at 65. The accumulation phase is your training ground. Use it.

What Volatility Means at 65

In retirement, the fear changes shape. It is no longer about a bad year. It is about watching your portfolio deplete while you withdraw from it.

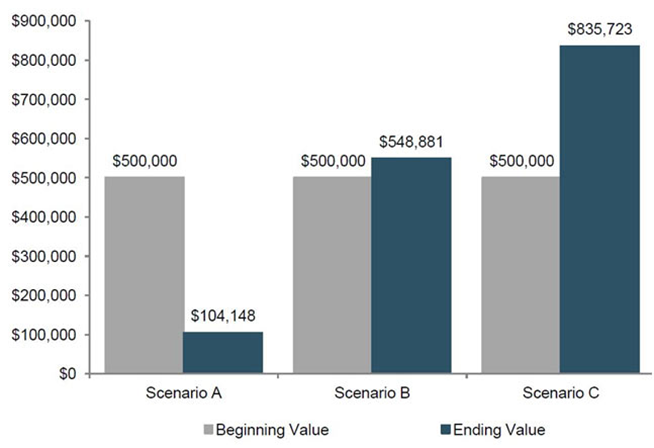

This is where sequence-of-returns risk shows up. Qtrade published a study a few years ago with three portfolios. Same starting balance ($500K). Same average annual return (5.40%) over 30 years. Same $21,000 annual withdrawal indexed at 2%.

Only the order of the returns changed.

Three identical averages. Three very different outcomes. The Scenario A, the retiree finishes with $731,000 less than the Scenario C retiree. Same math. Same withdrawal. Just bad luck on the timing.

This is what keeps retirees awake at 3 am. Not the drop itself. The drop combined with withdrawals.

The fix is not to hide in cash. That looks safe, but it kills your purchasing power over 30 years. The fix is to build a structure that lets you stop selling shares during downturns.

The Cash Wedge: Your Volatility Shield in Retirement

A cash reserve covering 24 to 36 months of withdrawals is the simplest defense against sequence-of-returns risk. When markets fall, you stop selling shares. You pull from the wedge. Your equities get time to recover.

One detail most retirees miss. The wedge does not need to cover 36 months of your full retirement budget. It only needs to cover the gap between what your portfolio generates and what you spend.

Budget $50,000. Portfolio generates $50,000 in dividends and interest. No wedge needed. Your income covers your spending.

Budget $50,000. Portfolio generates $30,000. A $20,000 gap. Three years of wedge means $60,000 in cash.

Budget $50,000. Portfolio generates $20,000. A $30,000 gap. Three years means $90,000 in cash.

The bigger the gap between income and budget, the bigger the wedge. The bigger the wedge, the lower your expected return. That is the price you pay to sleep at night. For some retirees, it is a fair trade.

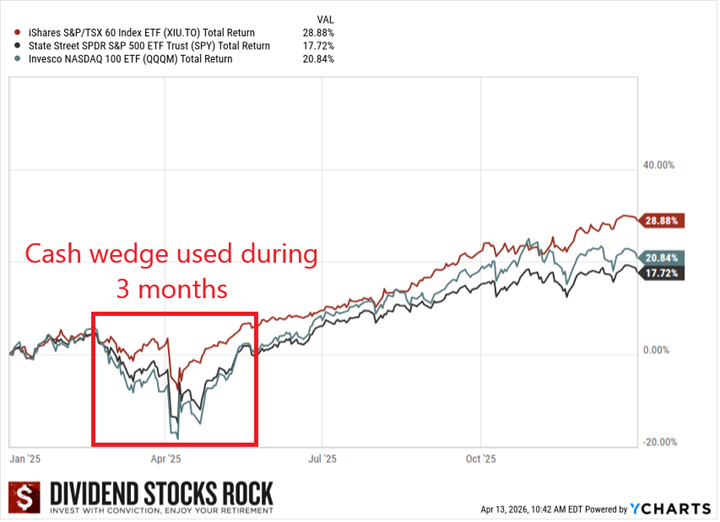

The 2025 tariff scare is a good example of the wedge in action. Markets dropped in February. They had fully recovered by May. Three months. A retiree with a wedge pulled from cash and never touched their equities. A retiree without one sold at the bottom and locked in the loss.

A GIC or bond ladder sits well alongside the wedge. Split a portion of your fixed income across one, two, three, four, and five-year maturities. Each year, one rung matures. You take what you need and reinvest the rest at the long end. It smooths your income and keeps you from chasing rates.

Want a bullet-proof retirement plan before summer?

If reading this section made you realize your portfolio is one bad year away from forcing painful choices, that is the gap Retirement Loop is built to close.

On June 2nd, we launch a 10-Day Bullet-Proof Plan program. I walk you through the mindset shift from accumulation to decumulation, the planning steps, and how to cover the risks that keep retirees up at night. Our retirement coaches will then review your finished plan for free.

Your plan will be done before you pack your bags for your summer trip.

The early-bird discount runs until Monday, June 1st, at $470 per year. After that, the doors close until further notice. Risk-free: 60-day money-back guarantee, no questions asked.

Join us at retirementloop.ca/join.

Three Rules to Stay Calm in a Drop

Understanding markets does not make you immune to panic. Loss aversion is wired into human brains. Behavioral finance research shows that a loss hurts about twice as much as the equivalent gain feels good. Losing $10,000 stings more than gaining $10,000 pleases.

These three rules let you act on logic when your gut wants to act on fear.

Rule 1: Separate price from value. A stock dropping 20% is a price event. Whether it is also a value event depends on the business. If the dividend triangle is intact and the business model is unchanged, the price drop is noise. This is why you build your investment thesis before you buy. You read it again when the price drops.

Rule 2: Pre-commit your response. Decide today what you will do if your portfolio drops 10%, 20%, or 30%. Write it down. When the drop comes, you execute a pre-made decision instead of inventing one under stress. Pre-committed rules beat real-time emotion almost every time.

Rule 3: Measure income, not price. During a downturn, check your dividend income instead of your portfolio value. If your holdings are still paying and raising their distributions, the portfolio is doing its job. The screen number is temporary.

None of this eliminates discomfort. A 30% drop still feels bad. The goal is to act rationally anyway.

Your Personal Volatility Stress Test

Run this checklist once a year, ideally in January, before you look at your annual return.

Cash reserve check. How many months of expenses does your wedge cover? Those below 6 months are vulnerable. 24 months is reasonable. 36 months handles most downturns.

Income concentration check. What percentage of your dividend income comes from your top three holdings? If one company accounts for more than 15% of your income, a dividend cut there will hurt your cash flow. Aim for no single holding above 10% of total income.

Core holdings check. What percentage of your equity portfolio sits in core holdings versus educated guesses versus falling knives? A retirement portfolio should be at least 80% in core holdings.

Sequence-of-returns check. Run the scenario. Markets drop 30% in year one of your retirement and stay flat for two years. Can you cover expenses from cash and fixed income without selling equities? If yes, you have protection. If no, that is the gap to close.

A Projections spreadsheet comes with the Retirement Loop’s membership. It is designed to test out such scenarios, only at the press of a button. Join us now.

Behavior check. Think back to March 2020 and 2022. Did you stay invested or did you make moves you later regretted? If you sold and missed the recovery, your current allocation is above your true volatility tolerance.

Conclusion

Volatility is the price you pay for equity returns over 30 to 40 years. There is no investment strategy that delivers stock-like returns without stock-like volatility. The math has never allowed it.

What changes between age 40 and age 65 is not the volatility. It is the cost of a bad reaction. At 40, a panic sale costs you years of compounding. At 65, it c

an mean running out of money.

Build the wedge. Stick to core holdings. Measure value, not price. The portfolio will look after itself.

If this is the year you want a retirement plan finished before your summer trip, the doors are open until Monday, June 1st. The 10-Day Bullet-Proof Plan kicks off June 2nd, and our coaches will review your work for free.

Early-bird is $470 for the year, with a 60-day money-back guarantee.

Join us at retirementloop.ca/join.

Leave a Reply