I often talk about Canadian financial stocks, especially banks, because they operate in what appears to be an oligopoly. To me, the best financial stocks are Canadian. That said, there are major US players that have proven to be excellent. Let’s dig into them.

Financials get a bad reputation in dividend portfolios. Some investors associate the sector with 2008. Others remember the 2023 regional bank failures. Many do not trust companies whose products they cannot describe in one sentence.

I get it.

But the sector is too important to ignore. Banks set the price of credit. Asset managers absorb pension and 401(k) flows. Stock exchanges and financial data firms power the modern market. Insurance companies underwrite the risks that the rest of the economy runs on. If you skip financials, you are skipping the engine room of capitalism.

The trick is to know what you are buying.

Below are my picks across four US financial sub-sectors. Each one scores well on the DSR PRO Rating and the Dividend Safety Score, and each one has a real reason to live in a long-term portfolio.

Disclosure: I own shares of Visa (V). I am a shareholder of Royal Bank (RY.TO) and National Bank (NA.TO) on the Canadian side. This is education, not advice. Do your own due diligence.

How I rank US financial stocks

I run every candidate through the same four-step checklist:

- DSR PRO Rating + Dividend Safety Score: I want both at 3 or higher, from a classic “hold” to solid fundamentals and a reliable dividend. A 5 means top of the class.

- Dividend Triangle: revenue growth, EPS growth, and dividend growth over five years. All three need to move in the same direction.

- Dividend history and streak: how long has the company raised the dividend without interruption? In financials, the streak matters more than in most sectors because of how often the cycle bites.

- Yield vs 5-year average: if the forward yield sits above the 5-year average, the stock may be undervalued.

No screener tricks. Just discipline.

Best US Banks

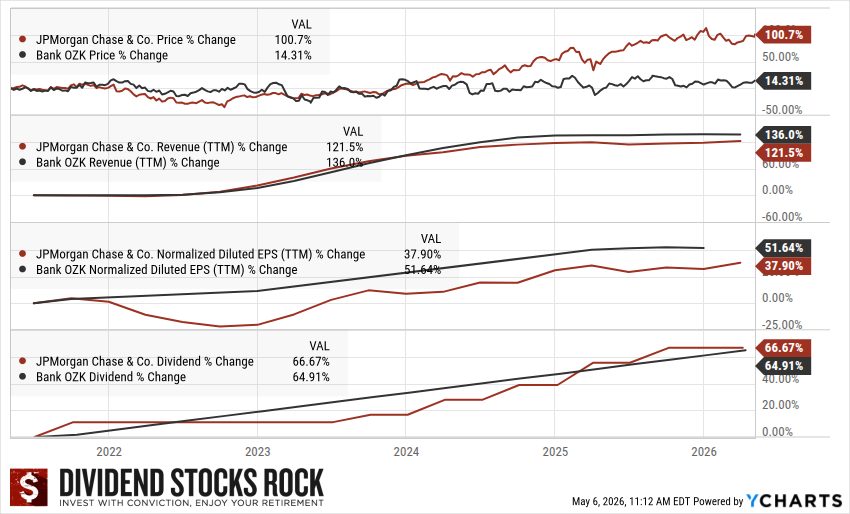

JPMorgan Chase (JPM): PRO 4 | Safety 4

Investment thesis: JPMorgan is the most dominant bank in the United States, leading in investment banking, commercial banking, credit cards, retail banking, and wealth management. The diversified model lets it capitalize on every part of the cycle and spread technology costs over a base of clients no competitor can match. Higher rates have driven record net interest income. Forward yield 1.90% (5-year average 2.35%), 15-year streak, payout 28.85%. JPM is the rare US bank I would want in a dividend portfolio.

Bank OZK (OZK): PRO 4 | Safety 4

Investment thesis: Bank OZK is a specialized regional bank led by CEO George Gleason since 1979. Its Real Estate Specialties Group runs disciplined construction and bridge lending on large commercial real estate projects, and the bank is scaling a Corporate and Institutional Banking division that has grown from 18 to 97 employees across 42 industry niches. Net interest margin sits at 4.20%, one of the strongest in regional banking. Forward yield 3.90% (5-year average 3.45%), 27-year streak, payout 28.35%. A regional bank with a dividend track record most US banks cannot match.

Best US Stock Exchange and Financial Data

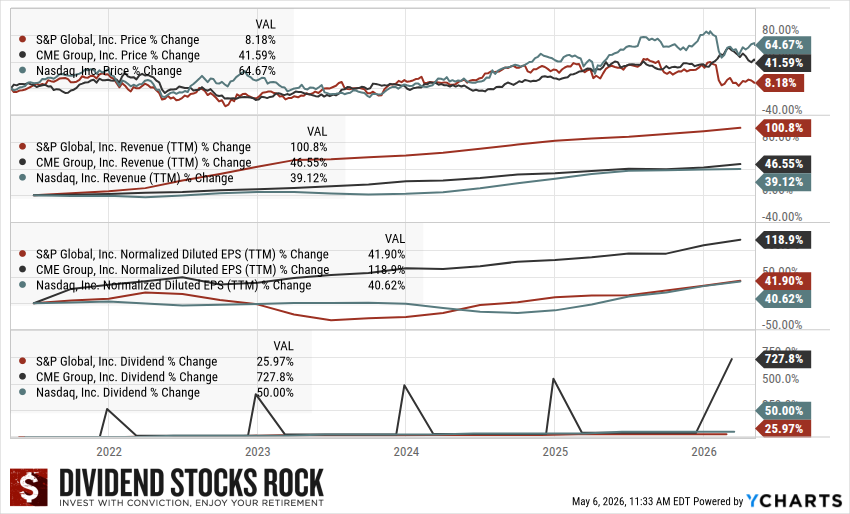

S&P Global (SPGI): PRO 4 | Safety 4

Investment thesis: S&P Global is the dominant financial information business in the world. Credit ratings, indices, market intelligence, and commodity insights live inside the financial system itself. The S&P 500 is licensed by every major ETF issuer. Forward yield 0.90% (5-year average 0.80%), 52-year streak (Dividend King), payout 26.15%. The longest streak in the group.

CME Group (CME): PRO 4 | Safety 4

Investment thesis: CME Group is the leading US derivatives exchange operator, with a near-monopoly in US futures and options across interest rates, equities, FX, commodities, and metals. CME holds a 27% stake in S&P Dow Jones Indices and is the exclusive venue for S&P futures trading. The dividend structure pairs a regular quarterly with an annual variable special, so the headline forward yield (0.00%) understates total cash return: the 5-year average yield sits at 2.05% and the 18-year streak shows total dividend growth even when the special varies. The most defensible balance sheet in the sub-sector.

Nasdaq (NDAQ): PRO 4 | Safety 4

Investment thesis: Nasdaq operates the actual exchange and a large analytics and anti-financial-crime software business. Listing fees provide recurring revenue, and the data + tech segments add pricing power. Forward yield 1.35% (5-year average 1.30%), 11-year streak, payout 33.60%. The cleanest way to own a US stock exchange.

Best US Insurance

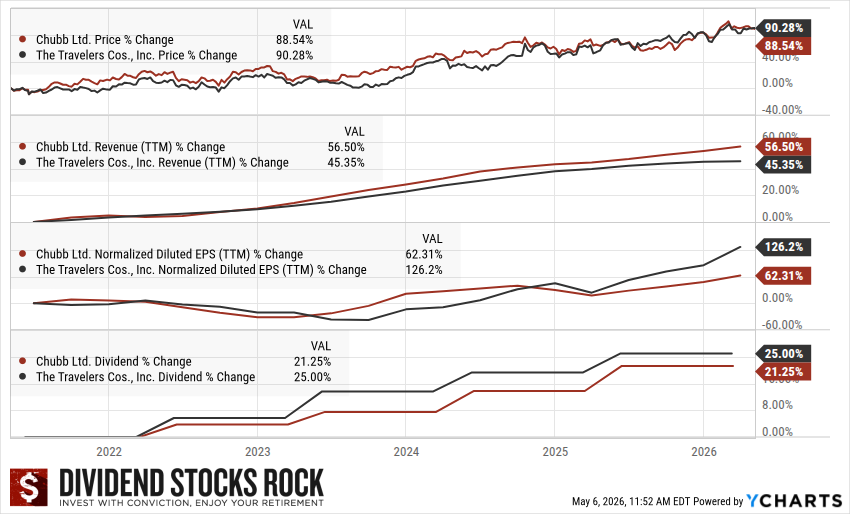

Chubb (CB): PRO 4 | Safety 4

Investment thesis: Chubb is the largest commercial property and casualty insurer in the world, with global reach and a focus on high-net-worth personal lines. The model is the closest US analog to Intact (IFC.TO), my preferred Canadian insurer. Forward yield 1.20% (5-year average 1.40%), 30-year streak, payout 14.75%, beta 0.44. Low yield, low beta, and a very conservative payout ratio.

H3: Travelers (TRV): PRO 4 | Safety 3

Investment thesis: Travelers is a pure-play US property and casualty insurer with strong commercial lines and personal auto exposure. Underwriting discipline has held up through hurricane seasons and the inflation cycle. Forward yield 1.65% (5-year average 1.85%), 21-year streak, payout 15.80%. A solid backup for investors who want US-only P&C exposure.

Best US Asset Managers

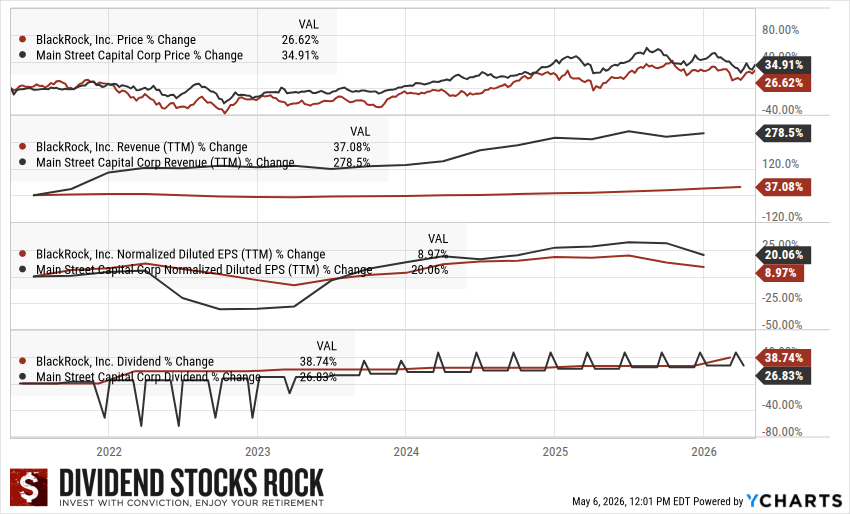

BlackRock (BLK): PRO 4 | Safety 4

Investment thesis: BlackRock is the largest asset manager in the world, with size and scale no competitor can match. The Aladdin technology platform adds a recurring software business inside the asset manager, and the 2024 Global Infrastructure Partners acquisition gave BLK a $150B+ private markets footprint. Forward yield 2.15% (5-year average 2.30%), 14-year streak, payout 58.80%. Management raised the dividend by 10% in 2026 after a quiet stretch.

Main Street Capital (MAIN): PRO 3 | Safety 3

Investment thesis: Main Street Capital is a Business Development Company that lends to and invests in lower-middle-market US companies. The model pairs a monthly distribution with annual special dividends, supported by an in-house underwriting team focused on first-lien senior secured structures and an exceptionally low operating-expense-to-assets ratio. MAIN compounded NAV through cycles and only missed a special dividend in 2020. Forward yield 5.60% (5-year average 6.05%), 13-year streak, payout 76.85%. The 3/3 rating reflects BDC structural risk: this is a yield play, not a sleep-easy stock.

Bonus: payment networks

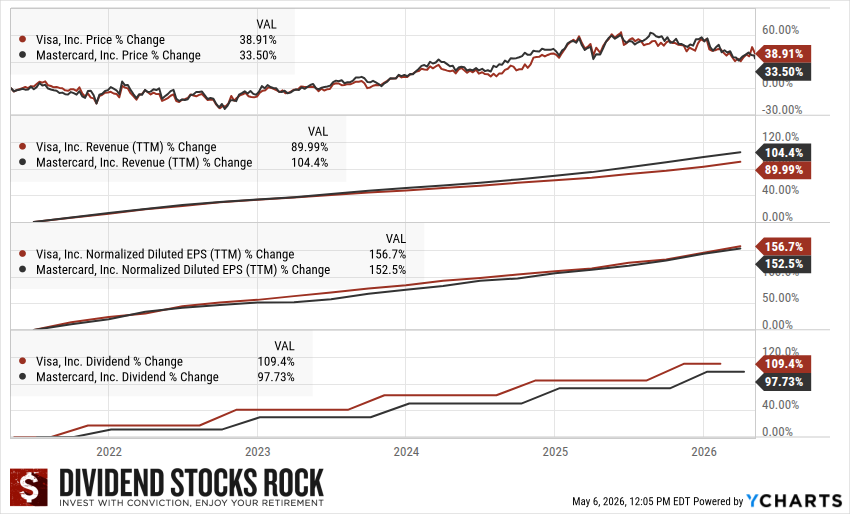

I cannot write about US financial stocks without flagging Visa (V) and Mastercard (MA). Both score PRO 5 / Safety 5: top of the class. They operate in a duopoly protected by global merchant adoption, and they are money-printing machines with very low capital intensity. Technically classified as Credit Services rather than banks or asset managers, but ignoring them in a US financial article would be a mistake.

Visa moves over $15 trillion in annual transaction volume across 200+ countries, with over 50% global market share. The asset-light model earns a fee on every swipe, tap, or click, with an operating margin of around 67% and an ROE of 52.75%. Forward yield 0.80% (5-year average 0.80%), 14-year streak, payout 23.35%. The moat sits in network effects across 14,500 financial institutions and over 50 million merchants.

Mastercard processed over $8 trillion in payments in 2024 and grows faster than Visa despite being the #2 player. ROE of 210.50% reflects the asset-light, low-capital-intensity model. Cross-border transactions remain the most profitable segment, and management is targeting 12% compound annual revenue growth through 2029, with cybersecurity (the $2.65B Recorded Future acquisition), tokenization (around 40% of transactions), and AI services layered on top. Forward yield 0.70% (5-year average 0.60%), 12-year streak, payout 18.95%.

The Ultimate Safe List to Get Dividend Growth Stock Ideas

To help you build a solid portfolio with dividend growth stocks, I have created the Dividend Rock Stars List, showing about 300 companies with growing trends.

You can read on to understand how it is built and why it’s the ultimate list for investors, or you can skip to the good stuff and enter your name and email below to get the instant download in your mailbox.

The verdict

Canadian banks and insurers remain my preferred dividend ideas in the financial sector. The oligopoly structure, the regulatory protection, and the long dividend track records are hard to beat.

But the US has real heavyweights worth owning. JPMorgan for banks. S&P Global for the financial data and exchange angle. Chubb for global property and casualty insurance. BlackRock for asset management. And Visa or Mastercard, if you want a money-printing machine on top.

Your portfolio has finite room. Pick the one or two names whose thesis you actually understand, then hold them long enough for the dividend growth to do its work.

Leave a Reply