When investors look at insurers, they often see large balance sheets, generous dividends, and stable businesses. At first, Intact Financial, Great-West Lifeco, Manulife, and Sun Life look like they belong in the same bucket.

But when digging deeper, there are differences to consider.

These four insurers don’t grow the same way, they don’t take the same risks, and they won’t appeal to the same type of investor. One dominates property and casualty insurance with disciplined underwriting. One leans more toward steady retirement and wealth businesses. One offers more upside through Asia. One has built a more balanced platform across insurance, group benefits, and asset management. On the surface, they all look solid. Under the hood, each has a very different personality.

That’s why this is such a useful stock battle. It’s not really about finding a “perfect” insurer. It’s about understanding which one fits your portfolio best.

If we turn this into a ranking of the best Canadian insurance stocks for dividend growth investors, this is where I land: Intact Financial first, Sun Life second, Great-West Lifeco third, and Manulife fourth. That ranking reflects the full picture: business model, earnings resilience, growth profile, and how comfortably each insurer fits inside a long-term dividend growth portfolio.

Four Insurers, Four Different Engines

All four companies operate in financial services, but they don’t rely on the same models.

Intact Financial (IFC.TO) is the one that stands out from the list. While the others are mostly tied to life insurance, wealth, and retirement products, Intact is a property and casualty insurer. It operates across Canada, the U.S., and the U.K./Ireland through brokers, direct-to-consumer brands like Belairdirect, and commercial platforms. This is a business built on underwriting discipline, claims management, pricing accuracy, and risk selection.

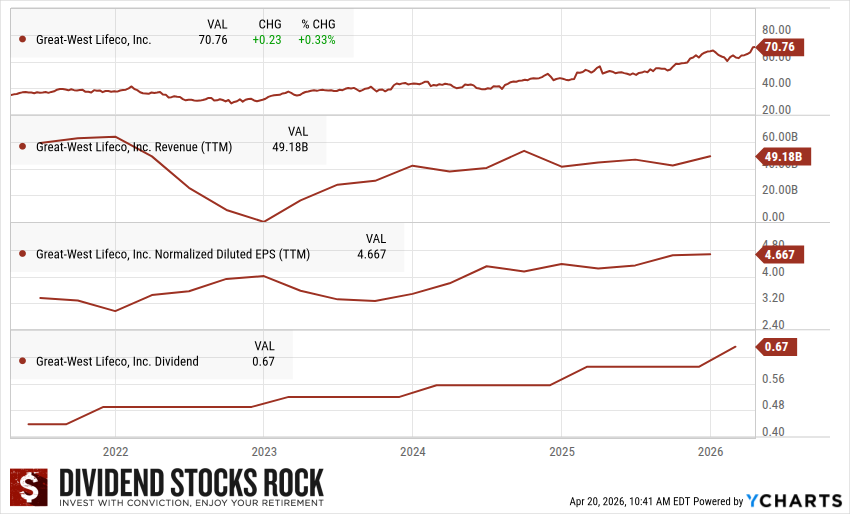

Great-West Lifeco (GWO.TO) is the most retirement-and-benefits-oriented of the group. Through Canada Life, Empower, and Irish Life, it has built meaningful exposure to insurance, wealth, pensions, retirement services, and reinsurance. Empower is the standout piece, giving Great-West a strong foothold in the U.S. defined-contribution market.

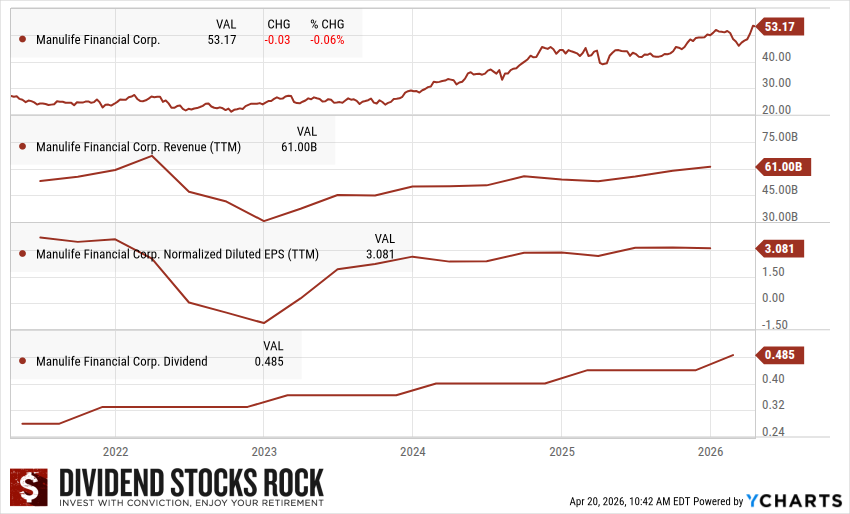

Manulife Financial (MFC.TO) is the most globally ambitious. It combines traditional insurance and annuity products with wealth and asset management, and its biggest growth driver is Asia. That gives it more upside potential than some peers, but it also adds more complexity and more sensitivity to market conditions.

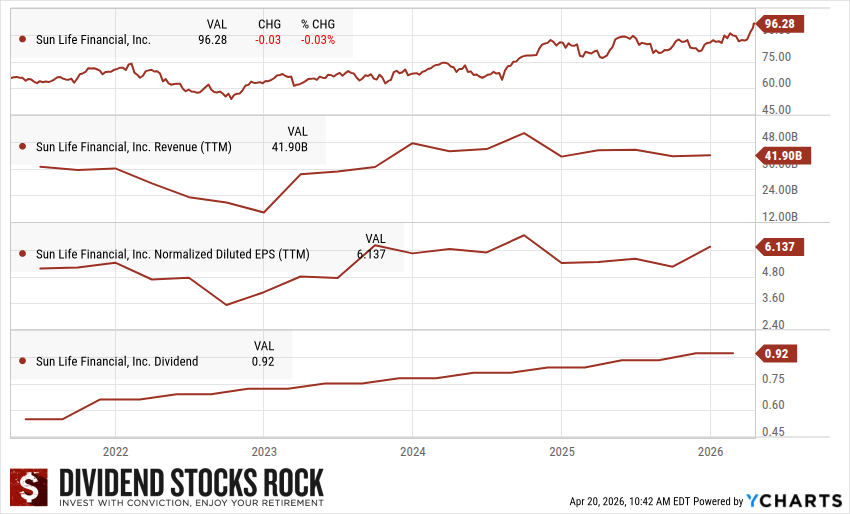

Sun Life Financial (SLF.TO) sits somewhere in the middle, and that is exactly why many investors like it. It has grown beyond traditional life insurance to offer asset management, wealth management, group benefits, health solutions, and protection products. It is probably the most balanced among the four life insurers.

If I had to summarize each one in a single line:

- Intact is the underwriting machine.

- Great-West is the retirement and benefits compounder.

- Manulife is the global growth story.

- Sun Life is the most balanced all-around life insurer.

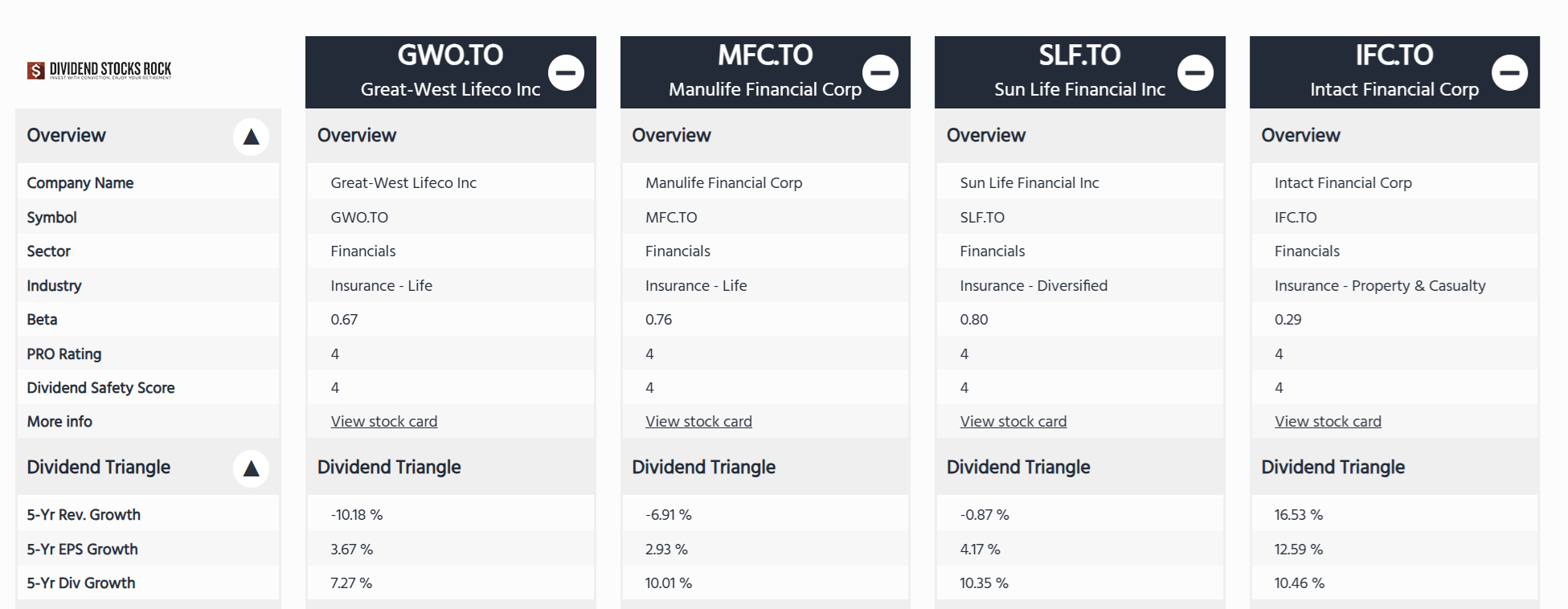

What the Dividend Triangle Tells Us

This is where the differences become much easier to spot.

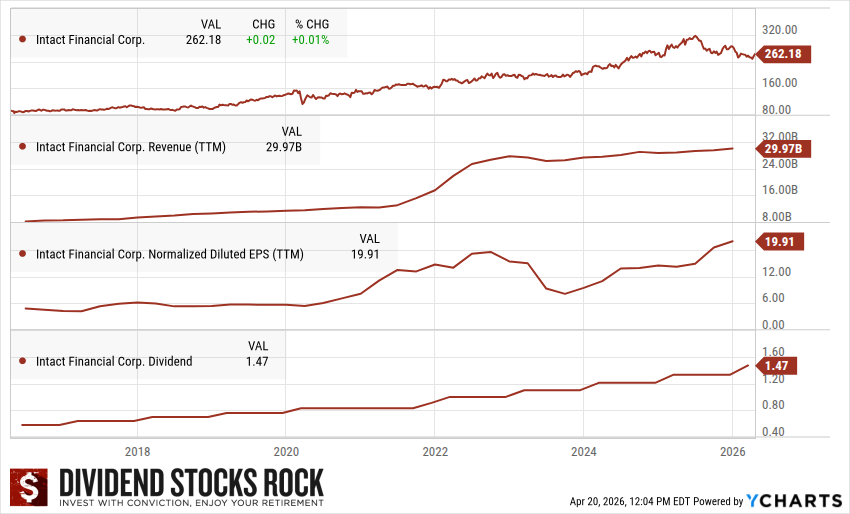

Intact is in a class of its own in this comparison. Its revenue, earnings, and dividend growth profile are meaningfully stronger than those of the three life insurers. That matters because it shows Intact is not just a defensive insurer with a decent payout. It is also producing real business momentum.

Sun Life comes next and stands out as the strongest of the life insurers. It shows the best balance between earnings growth and dividend growth, while its broader business mix helps reduce its dependence on any one segment.

Great-West is more modest. You get a solid dividend, a dependable business, and exposure to sticky retirement and benefits operations. But the growth runway is narrower, and most of its opportunities lie in mature markets.

Manulife still offers respectable dividend growth, but its earnings profile is less stable, and the business carries more execution risk. That does not make it a bad stock. It just makes it a different kind of fit.

These are capital-intensive businesses, and the real question is who can combine income, resilience, and enough growth to reward you for holding through a full market cycle.

#1 Intact Financial: The Best Overall Insurance Stock

Intact takes the top spot because it combines something dividend investors rarely get all at once: quality, growth, resilience, and consistency.

Its biggest advantage is that it plays a different game. Property and casualty insurance is not the same business as life insurance. Success depends on pricing risk properly, managing claims efficiently, and maintaining underwriting discipline year after year. That is where Intact shines.

The company has built a dominant position in Canada and has expanded intelligently into the U.S. and the U.K. through acquisitions such as OneBeacon and RSA. It now benefits from a broad product suite, diversified geography, and multiple distribution channels. BrokerLink, Belairdirect, affinity partnerships, and commercial platforms all strengthen the model.

Intact also has a data advantage. As the largest P&C insurer in Canada, it can use claims data and pricing models to make better underwriting decisions. That edge is hard to replicate. Management has also been clear about its long-term objective: grow net operating income per share by 10%+ annually while maintaining strong returns across the cycle.

The bear case is not hard to find. Catastrophe losses are rising, and severe weather is becoming a more expensive reality. Regulation limits flexibility in some lines, especially auto insurance. Growth outside Canada also comes with integration risks and more competition.

Still, Intact remains the strongest of the four. It has the clearest edge, the best growth profile, and the most complete investment thesis.

Best for: investors who want the strongest overall insurance business and a high-quality dividend growth compounder.

#2 Sun Life: The Most Balanced Life Insurer

If Intact is the best overall insurance stock, Sun Life is the best life insurer in the group.

What makes Sun Life so compelling is its balance. It is no longer just a traditional insurer collecting premiums and hoping for favorable underwriting. Asset management, wealth, group benefits, health solutions, and insurance all contribute to the story. That creates multiple growth levers and more recurring fee-based revenue.

Its asset management arm is an important source of steady earnings. Its Canadian group benefits platform is strong. Its U.S. health and benefits operations broaden the base. Asia adds another avenue for growth. The result is a business that feels more diversified and more resilient than a classic life insurer.

Sun Life is not risk-free. It remains exposed to financial markets, interest rates, underwriting pressure, and acquisition friction. DentaQuest created some noise and reminded investors that even strong businesses can hit speed bumps.

Still, among the life insurers, Sun Life offers the most complete mix of stability, diversification, and dividend growth.

Best for: investors who want a core long-term insurance holding with a healthy mix of income, moderate growth, and business diversification.

A Great Place to Find More Dividend Growers

If you like businesses with durable models, growing payouts, and strong long-term fundamentals, you should take a look at the Dividend Rock Stars List.

It’s a curated list built to help you find high-quality dividend growth stocks faster, without wasting time sorting through companies that don’t meet the mark. If you want proven dividend growers for your watchlist, this is a great place to start.

#3 Great-West Lifeco: The Steady Hand

Great-West is the kind of stock that rarely steals the spotlight, but it often delivers what conservative investors are looking for.

Its biggest strength is the quality of its business mix. Empower has become a major player in U.S. retirement services, while Canada Life and Irish Life provide dependable exposure to insurance, wealth, and benefits. Management has also been repositioning the business toward more capital-efficient and fee-driven operations, which is exactly the kind of move you want to see in a mature business.

The bull case is simple: Great-West has a dependable platform, strong cash flow generation, and sticky relationships in retirement and benefits. It does not need explosive growth to be a useful dividend growth holding.

The weakness is just as clear. Great-West has limited exposure to faster-growing regions, and its core insurance activities still operate in a highly competitive industry. Growth is harder to come by, and pricing power is limited.

That is why it ranks behind Sun Life. Great-West is dependable, but it is not as balanced and does not offer the same growth flexibility.

Best for: conservative dividend investors who want dependable income and a lower-drama financial stock.

#4 Manulife: The Upside Play With More Moving Parts

Manulife finishes fourth, but that does not mean it should be ignored.

In fact, Manulife may be the most interesting name here for investors looking for a bit more upside. Its Asian operations provide exposure to underpenetrated insurance markets and a rising middle class. Add its wealth and asset management operations, along with its strategic push into private credit and other international initiatives, and you can see why the long-term story still attracts attention.

If everything goes right, Manulife could deliver stronger growth than Great-West and maybe even challenge Sun Life.

But there is more baggage here, too.

Manulife is more sensitive to capital markets. Its earnings profile can be more volatile. Competition in Asia is intense. Its U.S. operations have not always delivered the returns investors would like. And unlike Great-West and Sun Life, Manulife still carries the memory of its 2008 dividend cut.

That history matters in a ranking designed for dividend growth investors. It is not disqualifying, but it is part of the picture.

Best for: investors who want a higher-growth angle, more international exposure, and are comfortable with a bumpier earnings path.

So, Which Insurer Wins?

The honest answer is that each one wins for a different type of investor.

If your priority is the strongest overall insurance company, Intact Financial deserves the crown.

If you want the best balanced life insurer, Sun Life gets the nod.

If your priority is dependable income and a steadier business model, Great-West Lifeco is a very good fit.

If you want more growth potential and can accept more variability, Manulife offers the highest ceiling.

When I look at a stock battle like this, I do not want to get trapped by yield. That is the fastest way to miss what really matters. These four all offer respectable income, but the better question is this: which business do you want to own for the next decade?

For the most conservative investor, Great-West makes a lot of sense. For an investor seeking a more global growth runway, Manulife stands out. For the investor building a classic dividend growth portfolio and looking for the most rounded life insurer, Sun Life looks like the cleanest fit. But if you want the best combination of business strength, underwriting discipline, growth, and long-term execution, Intact comes out on top.

In other words, this battle does not give us one weak name to avoid. It gives us four solid contenders, each with a different role to play.

But if we rank them today, the order is clear: Intact #1, Sun Life #2, Great-West #3, and Manulife #4.

Build a Better Watchlist

Want more stocks like these?

The Dividend Rock Stars List helps you find companies with strong dividend growth potential, proven business models, and the kind of fundamentals that can support long-term wealth creation. It’s one of the easiest ways to build a smarter watchlist and focus your research on names worth owning.

Conclusion

Canadian insurers may look similar from a distance, but they are not interchangeable.

Intact stands above the group thanks to its underwriting edge and stronger growth profile. Sun Life offers the most balanced life insurance platform. Great-West remains a steady and dependable choice for income-focused investors. Manulife brings more growth ambition, but also more moving parts.

That is what makes this sector interesting. You are not choosing between good and bad. You are choosing among different strengths, risks, and portfolio roles.

And when you understand that, picking the right insurer becomes a lot easier.

Leave a Reply