Many investors approach retirement income with the same question:

“How much yield can I get?”

It sounds logical. After all, if the goal is income, the natural reflex is to look for the biggest dividend stream possible. But that question often leads investors in the wrong direction. A high yield may look attractive today, but it does not guarantee safety, growth, or sustainable retirement income.

In fact, the opposite is often true.

Investors who focus too much on yield can easily end up holding slower-growth businesses, stretched payout ratios, or companies the market already sees as vulnerable. That’s why the best dividend investors eventually become yield agnostic. They stop obsessing over the size of the yield and start focusing on the quality behind it.

That shift makes all the difference.

Yield Is Just the Surface

A stock yielding 5% is not automatically better than one yielding 2%. It simply means more cash is being sent to shareholders right now. That’s it.

The real question is whether the business can support that payout while still growing.

That’s why my approach has evolved over the years. Even though the entire brand is built around dividend investing, the process itself is yield agnostic. The focus is not on whether a company yields 0.5%, 2.5%, or 5%. The focus is on whether the investment thesis is strong and whether the Dividend Triangle shows the right trends: revenue, earnings, and dividends moving up over time.

That’s a much better way to build income.

When you focus on quality first, you stop rejecting great companies just because they start with a lower yield. You also avoid being seduced by a fat yield that may be masking weak growth, poor execution, or rising risk.

Sustainable Income Comes From Business Strength

Many retirees want to “live off the dividends” and never touch their capital.

That’s understandable. It feels cleaner. Simpler. Safer.

But the truth is, your income is a function of your portfolio’s total return, not just the current yield it throws off. If your holdings do not generate enough returns over time, your income plan becomes fragile. If the underlying businesses stop growing, your dividend stream becomes exposed. If they run into trouble, cuts can happen. In other words, sustainable withdrawals only work when the portfolio generates enough total return to support them.

That’s why yield alone is never enough.

A high-yield portfolio built on weaker businesses can disappoint quickly. A portfolio of stronger dividend growers, even with a lower starting yield, often gives you a much better shot at creating reliable income through a mix of dividend growth, capital appreciation, and flexibility in retirement.

This is especially important when markets get rough. Dividends and distributions are not magically immune to business pressure. If the market can punish stock prices, companies can also reduce payouts. That’s why retirees should not confuse a high current yield with a safe income plan.

The Yield Agnostic in Real Life: National Bank vs. Scotiabank

A good way to illustrate this is to compare National Bank (NA.TO) and Scotiabank (BNS.TO).

Both are solid Canadian banks. Neither is a bad business. But if you were screening only for yield, you would likely choose Scotiabank first. It offers a more generous yield, which makes it look more attractive to income investors on the surface.

That’s where yield chasing can lead you astray.

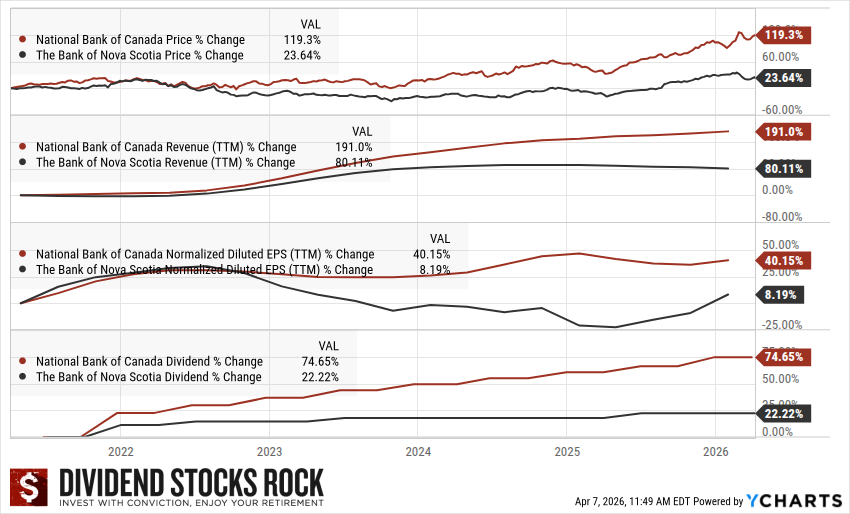

When you compare both banks through the Dividend Triangle, National Bank clearly comes out ahead. The chart below shows stronger share price performance, much stronger revenue growth, far better EPS growth, and much stronger dividend growth for National Bank over the period shown. Scotiabank offers a higher yield, but National Bank shows stronger business momentum.

That distinction matters.

National Bank has built a stronger growth profile by diversifying beyond traditional banking. It has expanded in wealth management, capital markets, and alternative lending, while keeping a dominant position in Quebec. Its acquisition of Canadian Western Bank should further broaden its footprint outside Quebec and create new cross-selling opportunities, particularly in private banking. It also continues to benefit from growth vectors like ABA Bank in Cambodia, Credigy in the U.S., and its Private Banking 1859 platform.

Scotiabank tells a different story.

Its international presence is often presented as a long-term advantage, particularly in Latin America. In theory, that should create stronger growth opportunities than a more domestic-focused bank. In practice, it has also brought greater volatility, higher execution risk, and greater exposure to political, currency, and economic instability. Scotiabank has struggled for years to turn that international footprint into superior shareholder returns.

That shows up in the results.

National Bank has rewarded investors with stronger growth because it has executed better. Scotiabank has often paid investors higher yields because the market has assigned it a lower valuation and less confidence.

That’s the kind of difference yield-focused investors miss.

If you only look at today’s income, Scotiabank might seem like the obvious choice. But if you look at the quality of the business, its growth profile, and its ability to keep compounding over time, National Bank stands out as the stronger retirement holding.

This doesn’t mean National Bank is risk-free. It still has significant exposure to Quebec, and its faster growth profile carries some execution risk. Provisions for credit losses must also be monitored carefully. Scotiabank is still a respectable bank with a strong domestic franchise and meaningful wealth management operations. But when you compare the two side by side, one has the better yield and the other has the better business.

For long-term dividend investors, the better business usually wins.

Why Yield Agnostic Investors Win

Yield-agnostic investors widen their universe.

They don’t lock themselves into stocks yielding above 4%. They don’t dismiss low-yielding names automatically. They don’t treat yield like the main evidence of quality.

Instead, they ask better questions:

Is the company growing revenue?

Are earnings supporting the payout?

Is management allocating capital well?

Does the dividend keep rising?

Does the business have durable competitive advantages?

Can this company still thrive in five or ten years?

That mindset leads to stronger portfolios because it focuses on the source of the income, not just the amount distributed today.

And in retirement, that’s exactly what you want.

You want a portfolio built on resilient businesses. You want dividends backed by earnings growth. You want flexibility when markets are down. You want income that can last, not income that only looks good on a stock screener.

Final Thought: Don’t Buy the Highest Yield. Buy the Best Chances.

The investors most likely to succeed with dividend investing are not the ones chasing the highest payout.

They’re the ones buying the strongest businesses.

Yield matters, but it should never come first. When you focus on quality, the dividend trend, the payout ratio, and the Dividend Triangle, you put yourself in a much better position to avoid cuts and build a retirement income stream that can actually hold up over time.

A big yield can feel reassuring.

A great business is what makes that income sustainable.

And if you want to dig deeper into how to build a retirement strategy around dividend growth and sustainable withdrawals, download the Dividend Income for Life guide.

That’s where the real retirement income conversation begins.

Buying a dividend paying stock is just taking from the appreciation from the stock that would have occurred if you’d not received a dividend. Given that the compounding return would be better to not take a dividend.

1. The Mathematical Perspective (The “Free Lunch” Myth)

Mathematically, it is correct. A dividend is not “extra” money created out of thin air; it is a distribution of a company’s existing assets.

When a company pays a dividend, its share price drops by the exact amount of that dividend on the ex-dividend date. For example, if a stock is trading at $100 and pays a $2 dividend, the stock price becomes $98. You still have $100 in total value ($98 in stock + $2 in cash), but the company now has $2 less per share on its balance sheet to reinvest in growth.

2. The Compounding and Tax Factor

This is also correct that receiving a dividend can create a “drag” on compounding for two reasons:

Taxation: If the stock is held in a taxable account, you must pay taxes on that dividend in the year you receive it. If the company had instead kept that money and seen its share price appreciate, you wouldn’t owe taxes until you sold the stock (potentially years or decades later).

Reinvestment Friction: To keep compounding at the same rate, you have to manually reinvest that dividend (buy more shares), which might involve transaction fees or buying at a higher price later.