Some stock comparisons are easy. One company clearly has the stronger balance sheet, better growth profile, or more durable business model.

Visa and Mastercard are not that kind of comparison.

This is a battle between two elite businesses operating some of the best models you’ll find in the market. They both sit at the center of global commerce. They both benefit from the shift away from cash. They both generate tremendous margins. They both post the kind of Dividend Triangle that makes dividend growth investors pay attention.

So the real question is not whether Visa or Mastercard is a good business. They both are. The question is which one deserves a place in your portfolio right now.

Two Exceptional Businesses Built on the Same Foundation

Visa and Mastercard are often described as payment processors, but that definition doesn’t fully capture how powerful their model is. A better way to think about them is as toll roads for global transactions.

When a customer buys something and a merchant gets paid, Visa or Mastercard stands in the middle and helps move that money securely and almost instantly. They collect a fee for facilitating the transaction, but they do not hold the credit risk. That risk remains on the balance sheet of the issuing bank.

That’s what makes the model so attractive.

They benefit from the growth of card payments, digital wallets, contactless payments, e-commerce, and cross-border transactions without having to lend money directly. It’s an asset-light setup with tremendous scale. As transaction volume rises, revenue grows without a corresponding need for heavy capital investment. That’s how you end up with a business that is both margin-rich and highly scalable.

Both companies also enjoy multiple ways to grow. The world continues to move toward electronic payments. Cross-border spending remains a powerful tailwind. Emerging markets still offer plenty of room to convert cash transactions into digital ones. On top of that, both companies have expanded aggressively into value-added services such as fraud prevention, analytics, digital authentication, open banking, consulting, and payment gateways.

This matters because it gives them more than one engine of growth.

Why the Moat Is So Hard to Crack

Visa and Mastercard operate inside one of the strongest economic moats in the market.

Their network effect is massive. Consumers use them because merchants accept them. Merchants accept them because consumers carry them. Banks issue cards on their networks because that is where the scale already exists. It becomes a self-reinforcing loop that is incredibly difficult for a new competitor to break.

That moat is supported by high switching costs, global acceptance, technology infrastructure, regulation, and trust. It would take an enormous amount of capital, time, and coordination to build a realistic challenger with similar reach.

This is why both stocks often look expensive at first glance. The market usually assigns premium valuations to businesses with dominant market positions, powerful free cash flow generation, and very long growth runways.

The Key Differences Between Visa and Mastercard

Even though the two companies look very similar from a distance, the differences show up when you go one level deeper.

Visa is the scale leader. It has a larger footprint overall and a stronger position in the U.S. debit ecosystem. Its model leans more heavily toward consumer card spending and cross-border travel. It also has a superior margin profile, which gives it tremendous flexibility to absorb legal costs, continue investing in the business, and return capital to shareholders.

Mastercard, meanwhile, looks a bit more like the growth challenger. It has built a broader mix of value-added services and has historically leaned harder into partnerships, international markets, and digital-first initiatives. In several regions outside the U.S., Mastercard has carved out strong positions and often appears more aggressive in pursuing new opportunities.

That difference may sound subtle, but it matters.

Visa wins on scale and efficiency. Mastercard often wins on sharpness and diversification through services.

If I had to summarize it in one sentence, I’d say this: Visa is the scale machine, while Mastercard is the growth aggregator.

The Dividend Growth Case Is Hard to Ignore

This is where both companies become especially attractive for dividend growth investors.

Neither Visa nor Mastercard is a high-yield stock, and that’s perfectly fine. This is not about current income. This is about owning businesses that can grow revenue, earnings, and dividends year after year at an impressive pace.

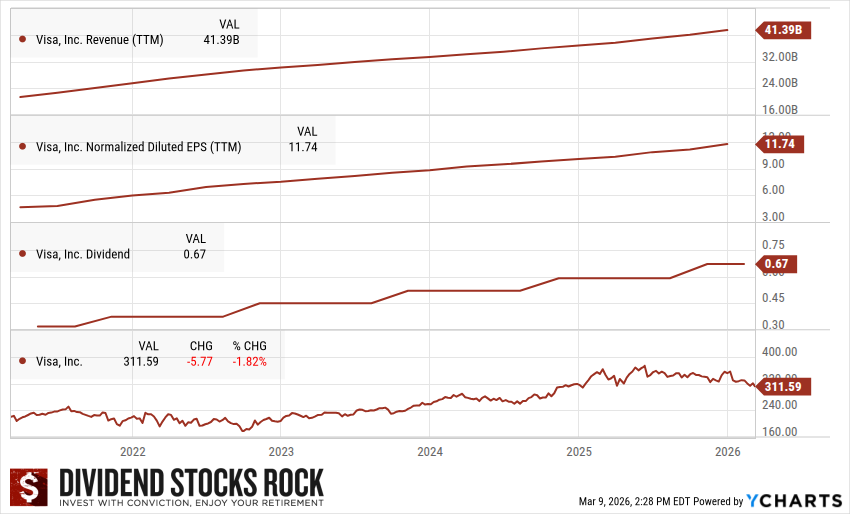

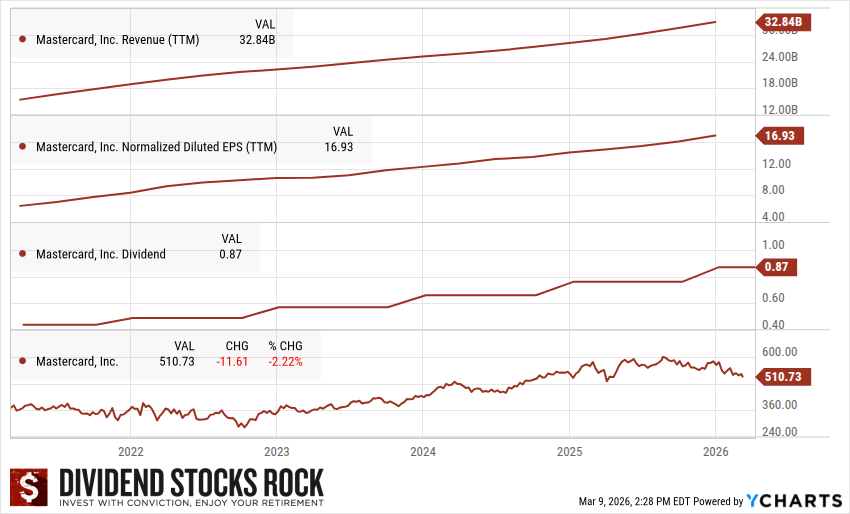

That’s exactly what their Dividend Triangles show.

Their payout ratios remain low, comfortably under 30%, which leaves plenty of room for future dividend increases. Their earnings growth supports those increases. Their revenue trends confirm the strength of the underlying business model. When all three sides of the triangle are moving in the right direction, you get the kind of setup that can compound beautifully over time.

Looking at the charts, both companies make a compelling case. Visa’s 5-year Dividend Triangle is exactly what you want from a best-in-class business: steady revenue growth, strong EPS progression, and a dividend climbing in a disciplined way. Mastercard shows the same pattern, with slightly stronger growth over the long term. That’s one reason many investors see Mastercard as the slightly more dynamic of the two, even though Visa remains the bigger player.

If you are building a portfolio around sleep-well-at-night dividend growers, both names deserve serious attention.

300 Stock Ideas With a Positive Dividend Triangle—Get the List Now!

I’ve used the Dividend Triangle to build a list of about 300 companies showing positive 5-year trends for revenue, EPS, and dividends.

The Dividend Rock Stars list is updated monthly and is a great starting point if you want to speed up your stock research.

Save yourself a ton of work—enter your name and email below and I’ll send it to you.

Why Have Visa and Mastercard Lagged the Market Recently?

This is the part that surprises investors.

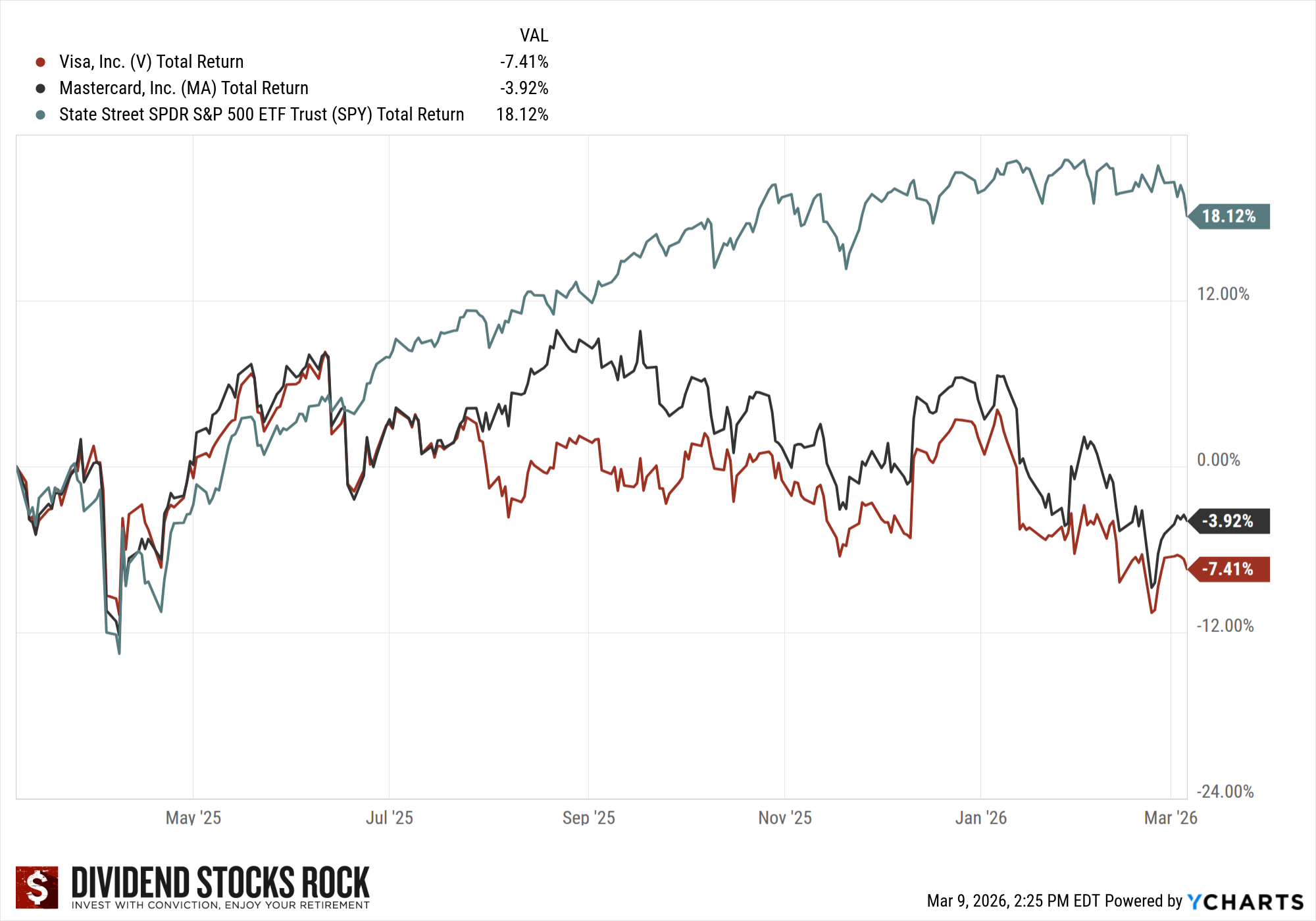

If these are such amazing businesses, why have both stocks lagged SPY over the past year?

Your comparison chart tells the story clearly. Over the last 12 months, SPY (following the S&P 500 market return) posted a strong gain while Visa and Mastercard both delivered negative total returns. Mastercard held up better than Visa, but neither kept pace with the broader market.

That underperformance does not mean the thesis is broken.

In fact, the explanation is fairly straightforward. A large share of recent market gains has been driven by mega-cap tech and AI enthusiasm. Visa and Mastercard are phenomenal businesses, but they are not viewed as the centerpiece of the AI trade. That means they haven’t enjoyed the same kind of multiple expansion.

At the same time, both companies continue to face recurring pressure from regulators and merchants over swipe fees and interchange. That is nothing new, but it remains a headline risk that weighs on sentiment. There is also the reality of tougher comparisons. Travel recovery and e-commerce tailwinds created a powerful rebound over the last few years. Now the growth rates look steadier, which is still good for business, but not always enough to excite the market.

Finally, valuation normalization matters. These stocks have often traded at premium price-to-earnings ratios in the mid-30s or higher. When that premium compresses closer to 30, the stocks can stall even if the business continues to perform well.

This is often the kind of setup long-term investors should pay attention to. Great companies rarely go on sale because their business breaks. More often, they become more attractive because expectations cool off.

The Risks Are Real, Even for Great Businesses

There is no such thing as a perfect stock.

For Visa and Mastercard, the biggest operational risk is global spending. People continue using cards in all kinds of environments, but transaction volumes can soften when consumers travel less, spend less, or delay discretionary purchases.

Regulation is another constant risk. Governments and legal bodies continue to examine fees, market dominance, and competitive practices. These issues are not new, but they can cap pricing flexibility and create uncertainty around future profitability.

Then there is competition. American Express, Discover, PayPal, fintech players, account-to-account payment systems, crypto infrastructure, and AI-enabled payment innovations all represent pressure points. None of them have cracked the moat in a meaningful way yet, but they are still worth watching.

Which One Would I Choose?

You really can’t go wrong with either one.

If you want the scale leader with superior margins, a dominant U.S. position, and a business that keeps printing cash with remarkable consistency, Visa remains a fantastic choice.

If you want the company with a slightly stronger long-term growth profile, broader service exposure, and a bit more edge in international and partnership-driven expansion, Mastercard may deserve the nod.

Personally, I see this as a classic quality-vs-quality decision. Visa offers comfort through scale. Mastercard offers excitement through slightly stronger growth.

For many investors, the right answer may simply be owning one of them and moving on. You don’t need to overcomplicate it when both businesses are this strong.

Final Thoughts

Visa and Mastercard are two of the best examples of what a premium dividend growth stock should look like. They have wide moats, high margins, scalable business models, and excellent Dividend Triangles. The recent underperformance versus SPY may look disappointing on the surface, but it may also be creating an opportunity.

Sometimes the market gives you a chance to buy exceptional businesses when the narrative cools down. This looks like one of those moments.

And if you want to find more companies with the same kind of strong fundamentals, the Dividend Rock Stars List is one of the best tools to get started. It gives you a focused list of companies with positive trends in revenue, earnings, and dividends, so you can spend less time screening and more time analyzing the best ideas.

MasterCard and Visa will not take over payments with cash in the developing world, mobile payments will, at least where there is sufficient mobile network coverage, which is all of Africa, most of America(s), and much of Asia. Most people in developing countries already own smartphones, most of them already use mobile phone payments to sometimes buy stuff via internet (often “money” accounts at different internet merchants, or service providers, like delivery services).

Much of the MasterCard and Visa marketshare in Europe will be replaced with pan-European payment solutions. But the profit from Europe will still increase, many will continue to use their old cards, and some young people will choose MasterCard or Visa, because the pan-European payment systems will likely not work outside Europe.